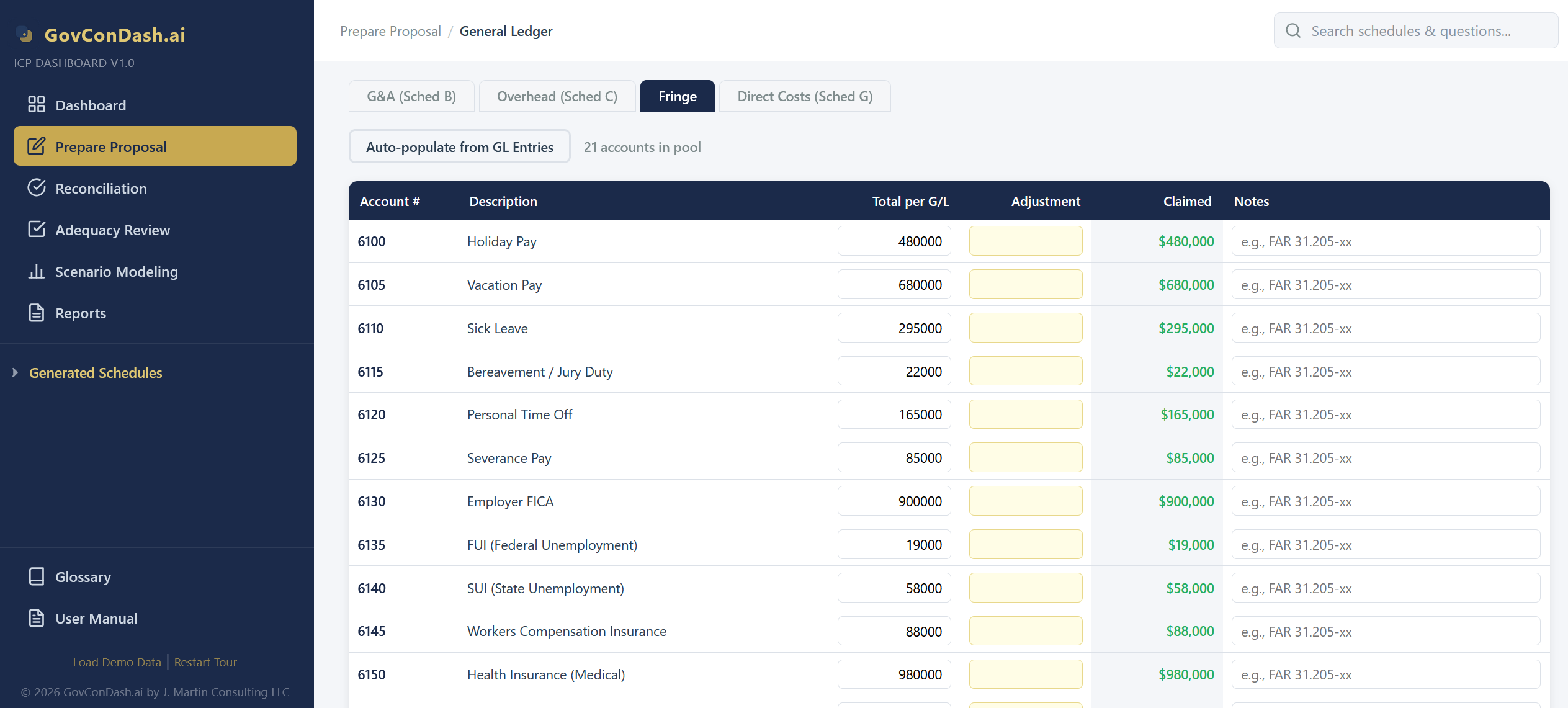

What Goes Into the Fringe Pool

Fringe accounts are easy to identify because they all share one characteristic: the cost is driven by labor, not by contract activity or company-wide management. The pool is built from payroll tax accounts, insurance accounts, retirement accounts, and paid-leave accounts.

- Payroll Taxes — Employer-paid FICA, Medicare, FUTA, and SUTA. These are mandatory and scale directly with gross wages.

- Health & Dental Insurance — Employer premium contributions for medical, dental, and vision coverage. Typically the largest component of the pool.

- Life & Disability Insurance — Employer-paid group life, short-term disability, and long-term disability premiums.

- Retirement Contributions — 401(k) employer match, profit-sharing, pension contributions. Must comply with FAR 31.205-6(j) deferred compensation rules.

- Paid Leave — PTO, holiday pay, sick leave, jury duty, and bereavement. Treated as fringe because the cost is incurred without corresponding direct work.

- Workers' Compensation — Premium costs for workers' comp insurance, typically allocated on a labor-dollar base.

- Adjustments — Unallowable compensation elements (excessive executive pay above the FAR 31.205-6(p) cap, certain bonuses, golden parachutes) are removed via adjustments.