Facilities Capital

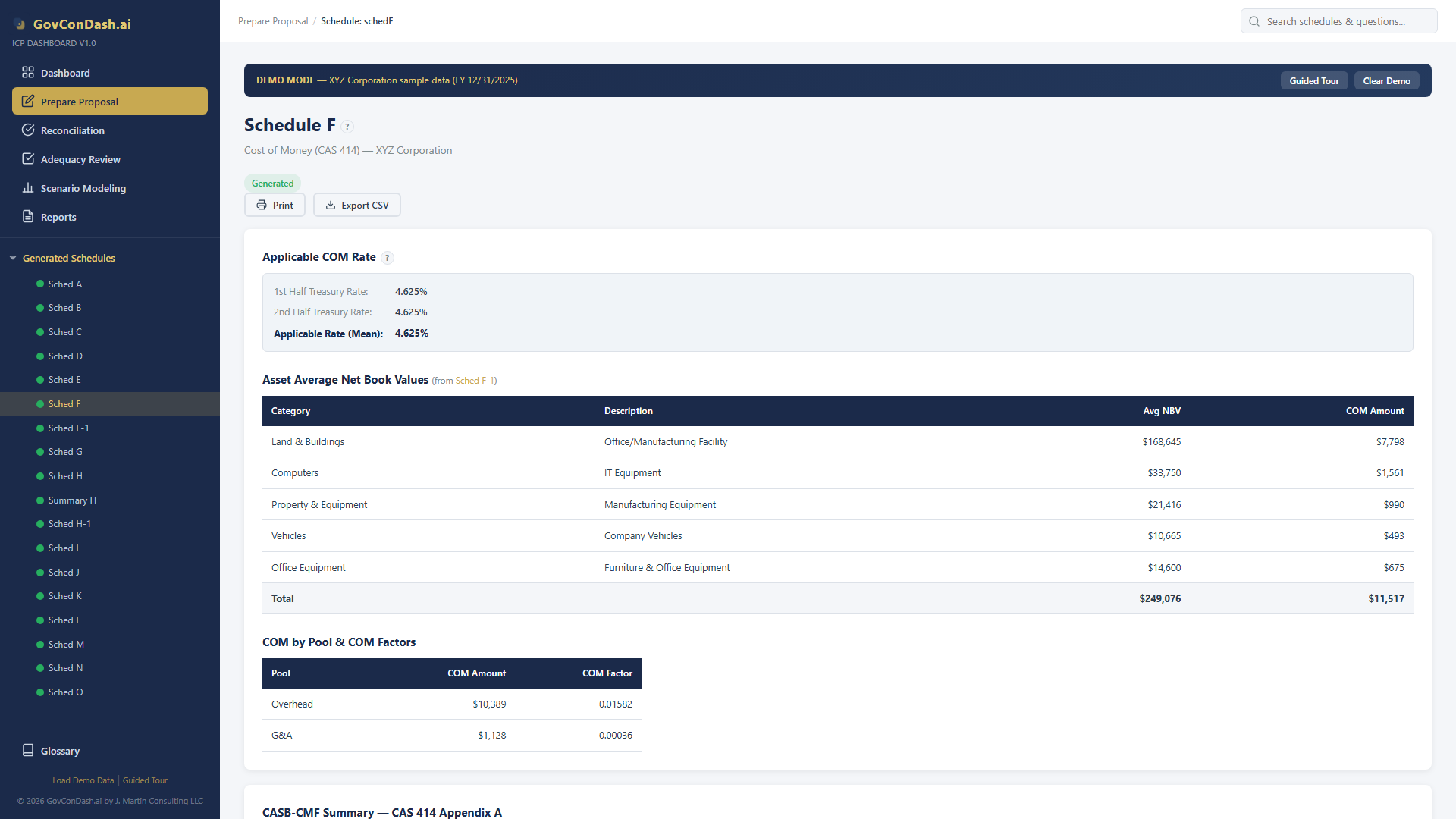

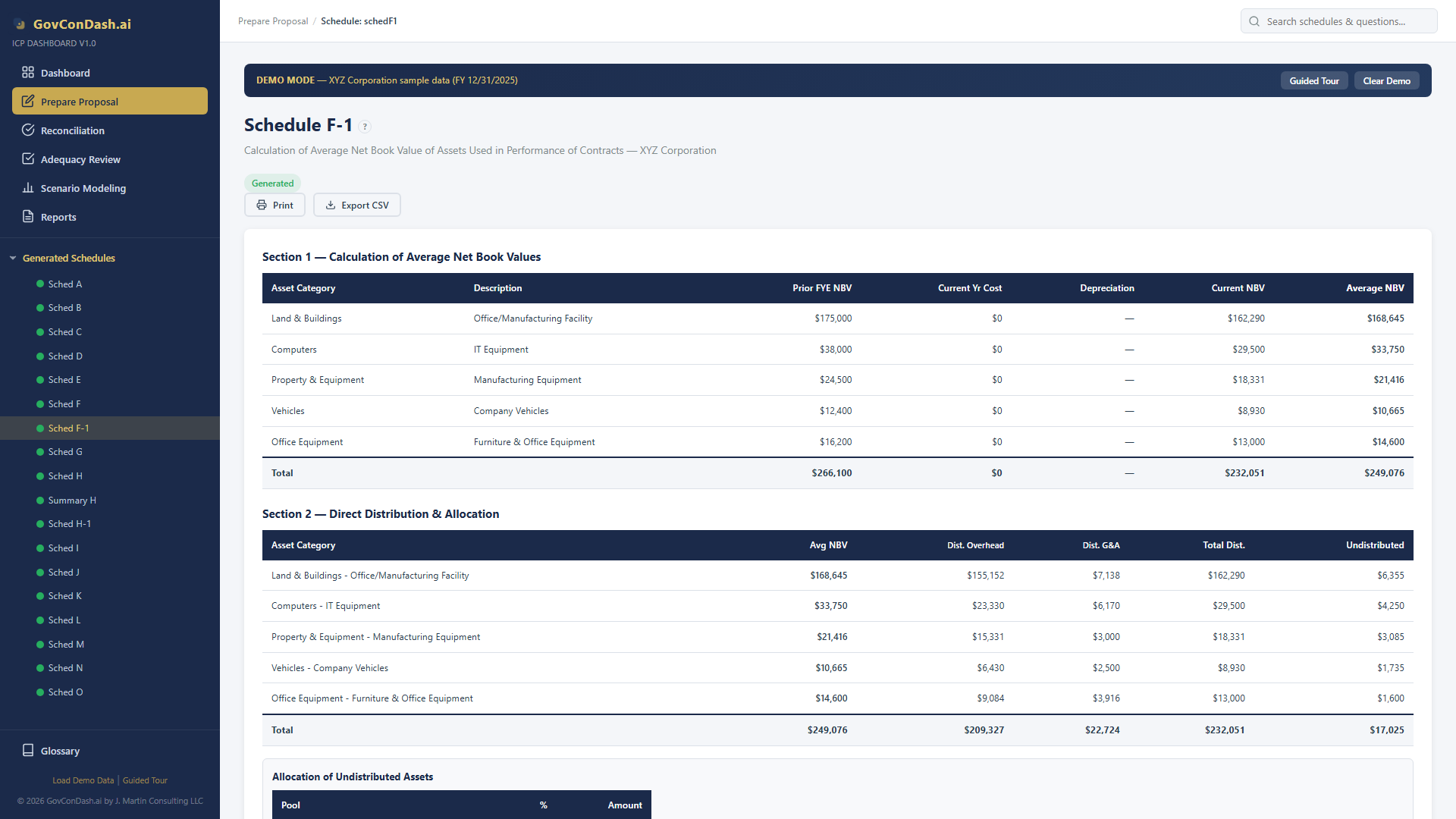

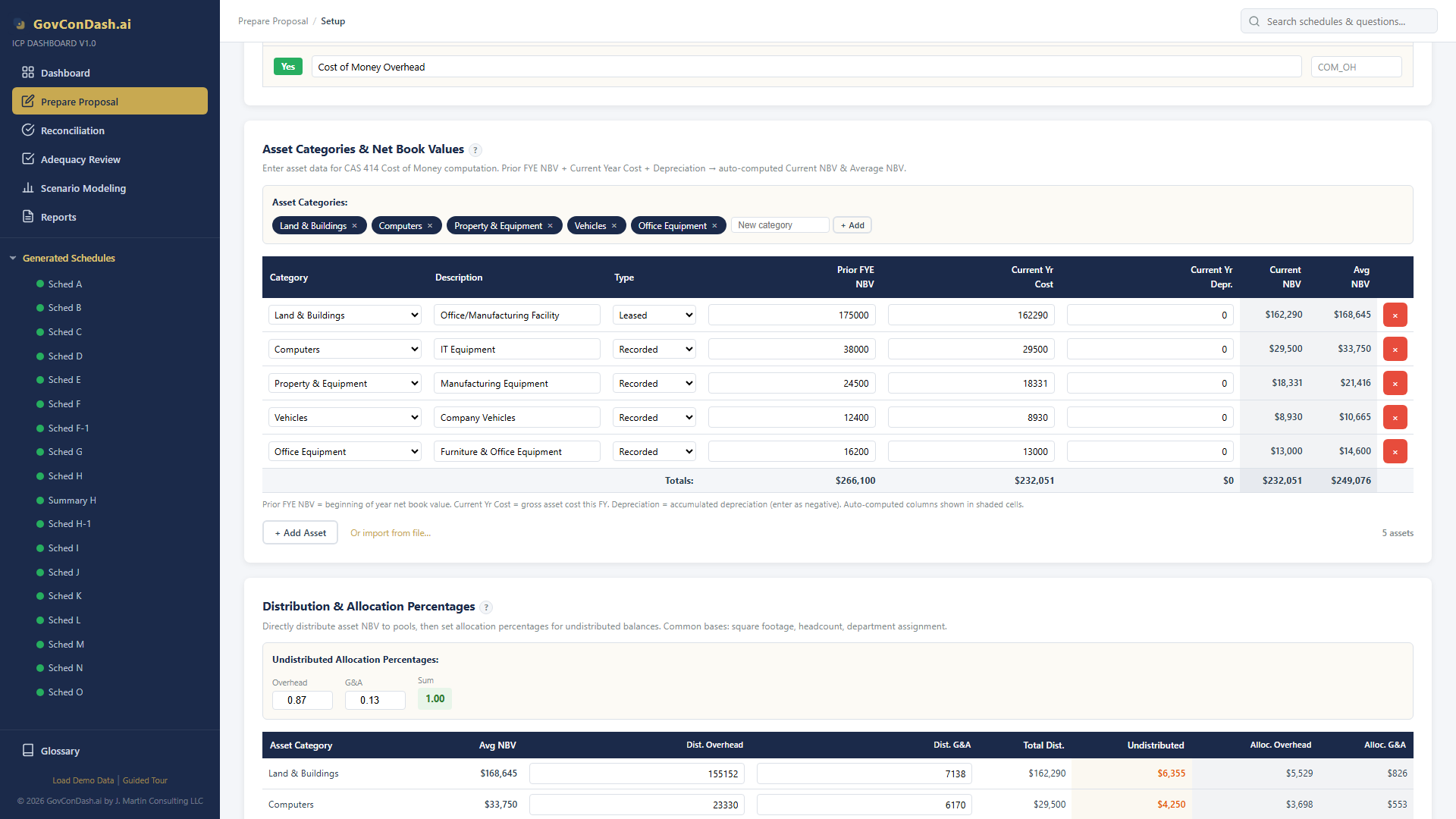

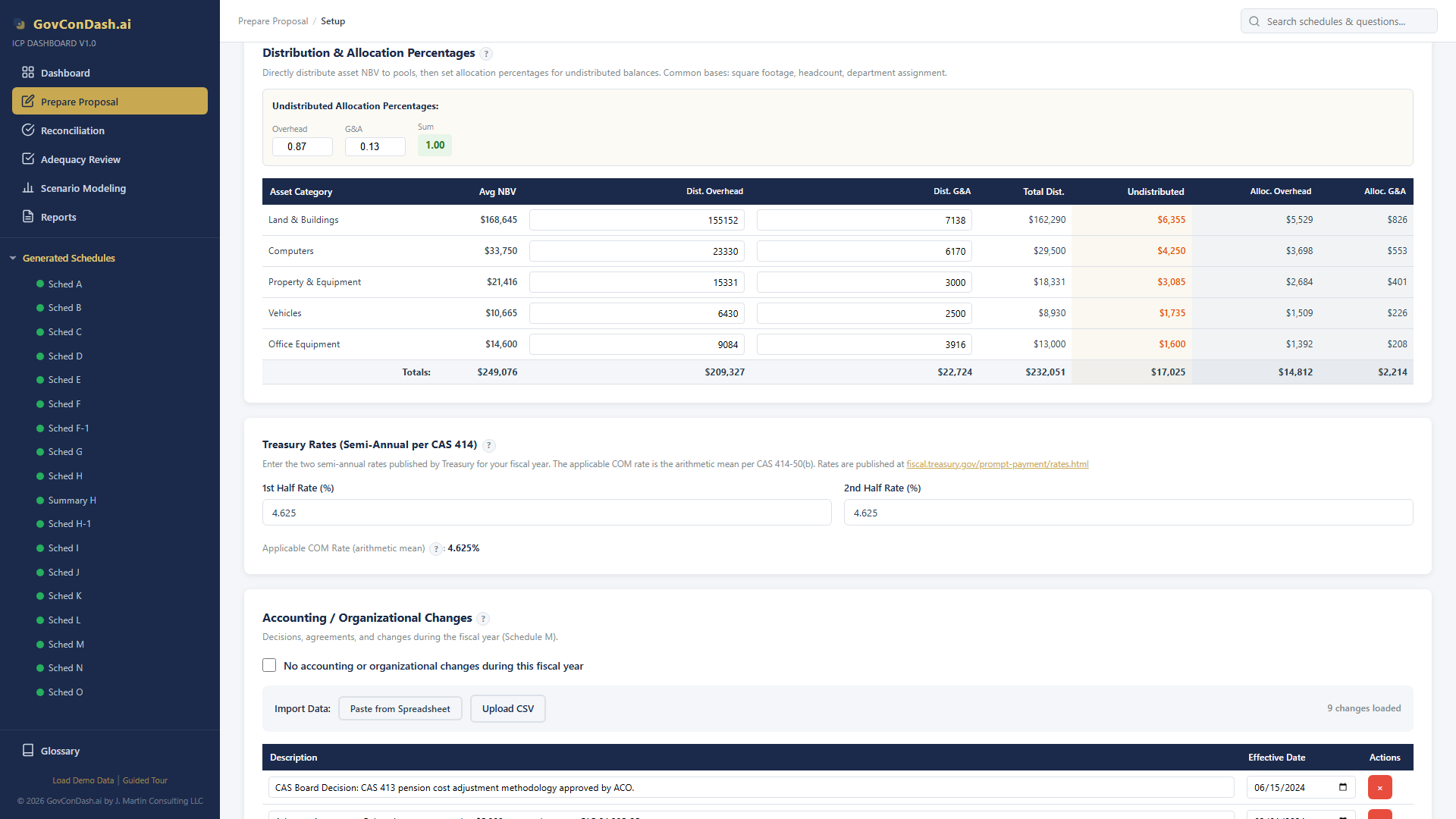

Cost of Money

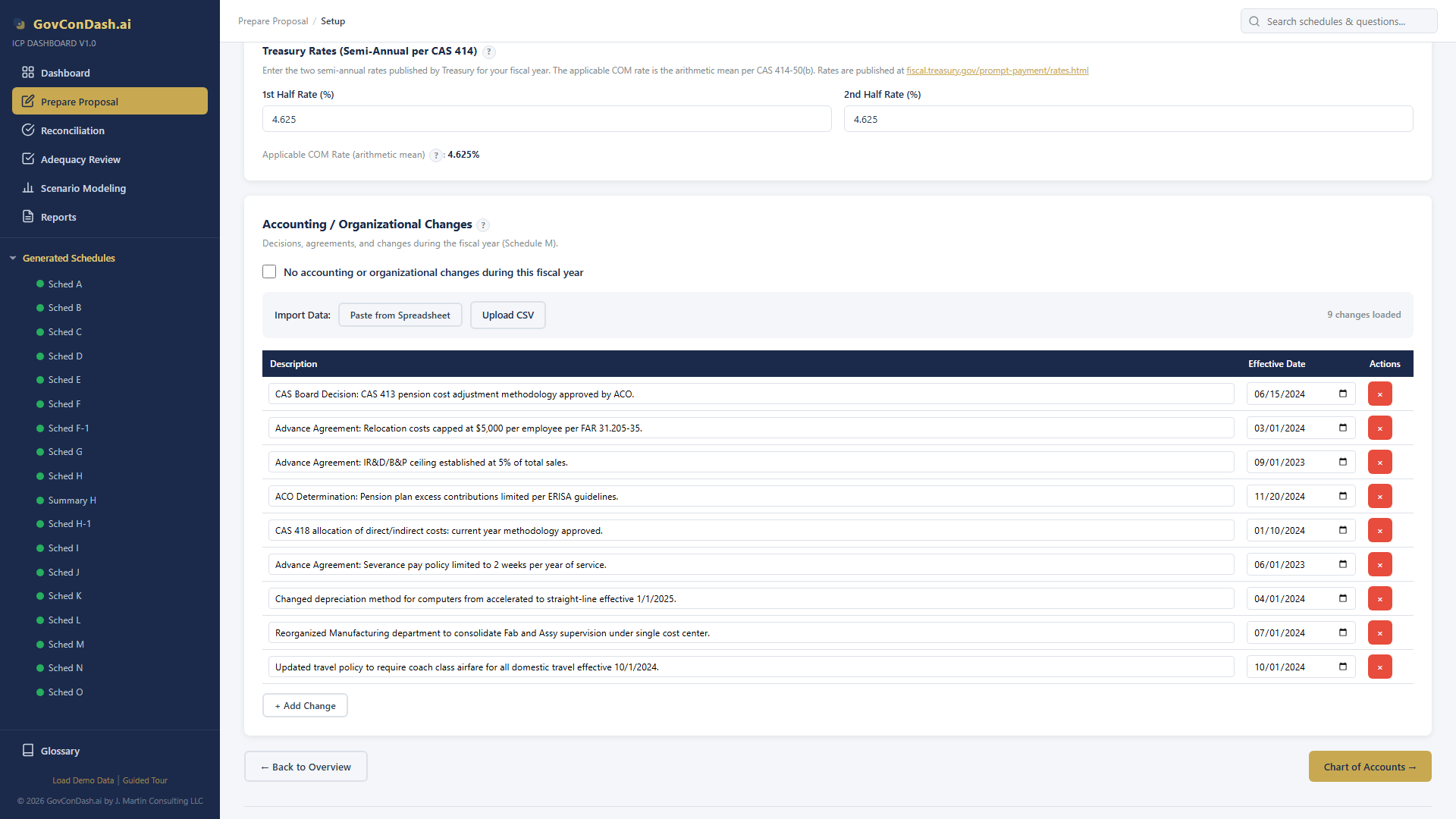

An imputed return on the assets you've invested in your business — recognized as an allowable contract cost under CAS 414 and reported on Schedule F of the incurred cost proposal.

CAS 414

Controlling Standard

DD 1861

FCCM Form

Sch F

ICP Computation