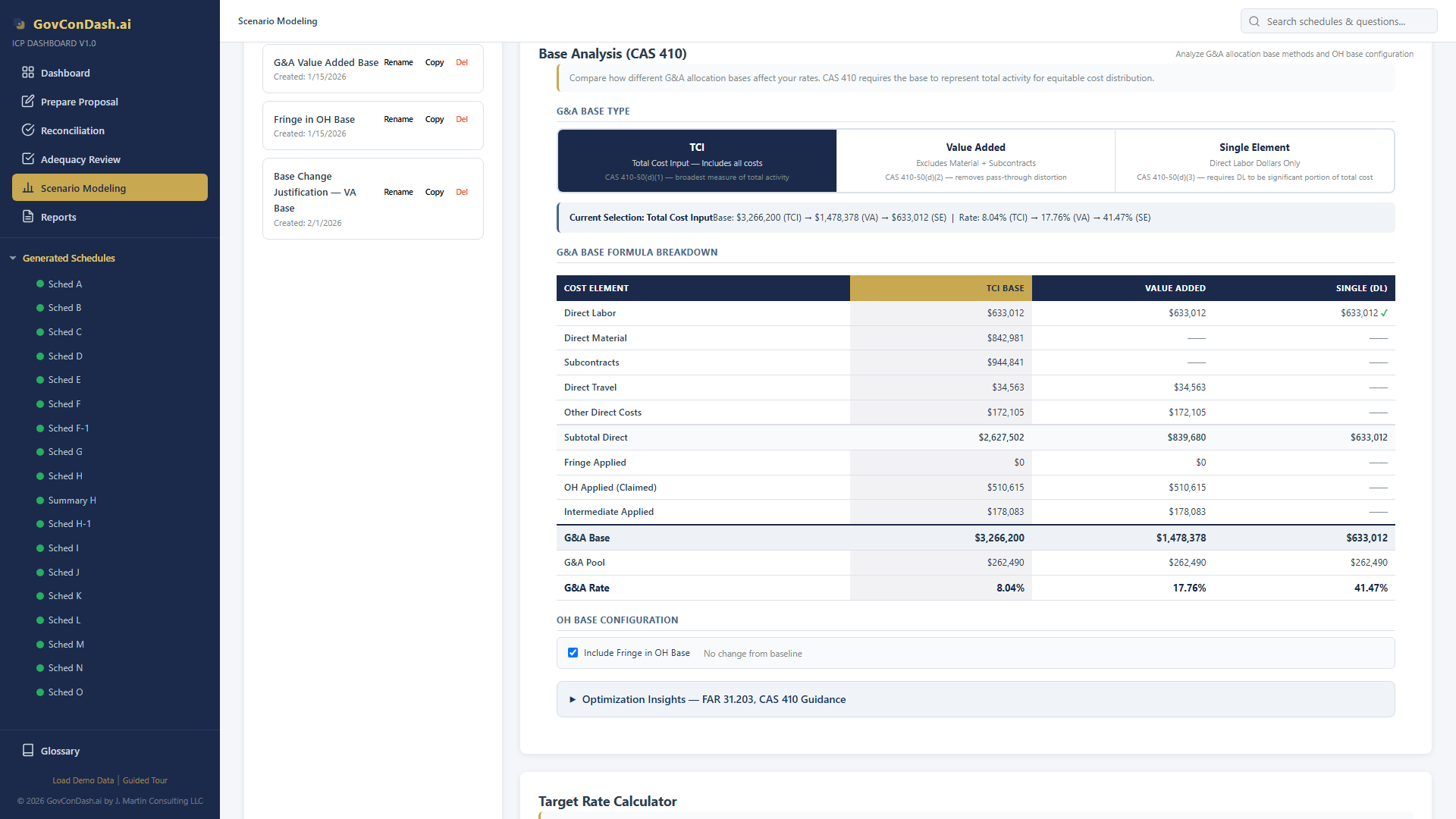

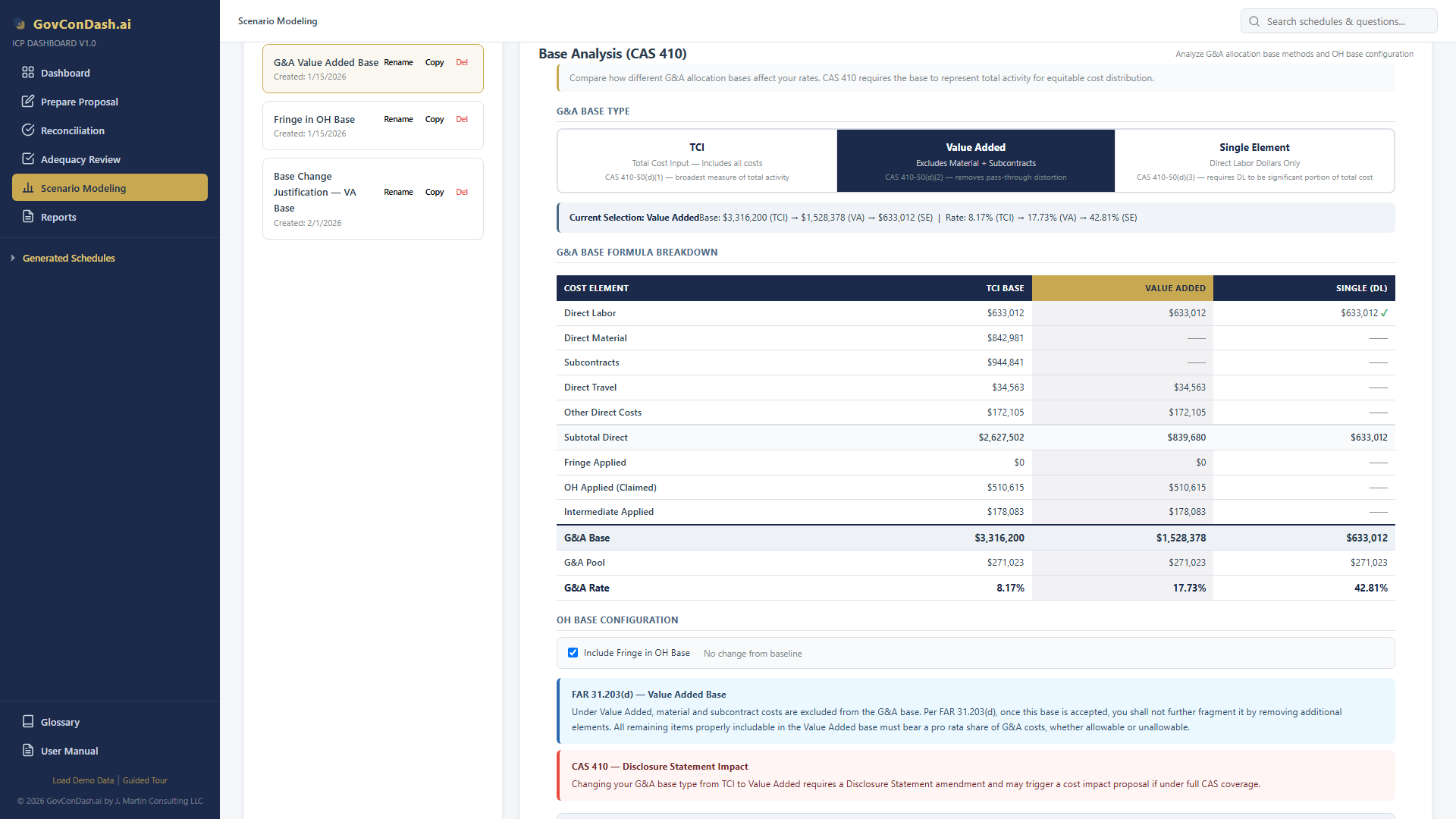

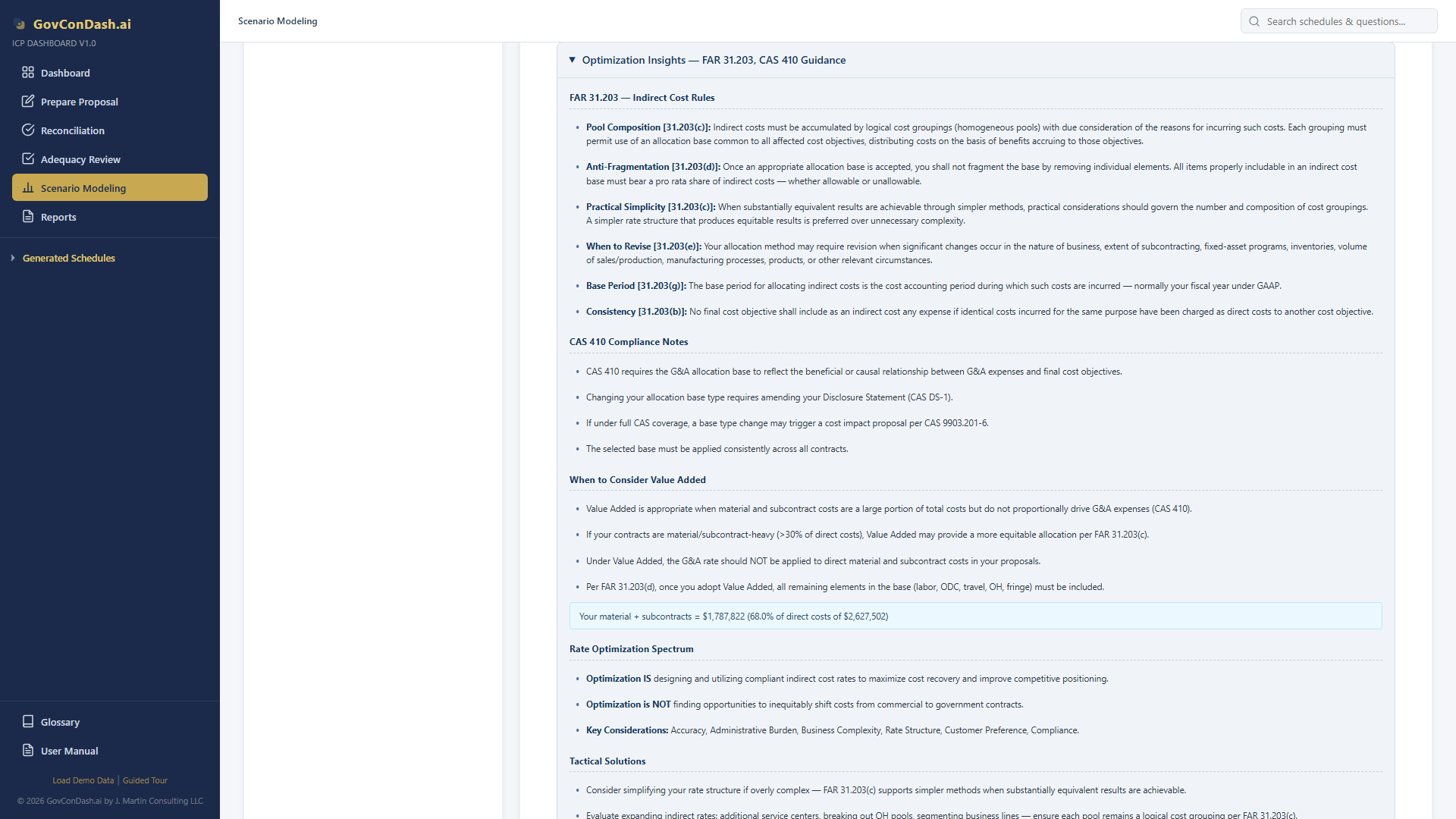

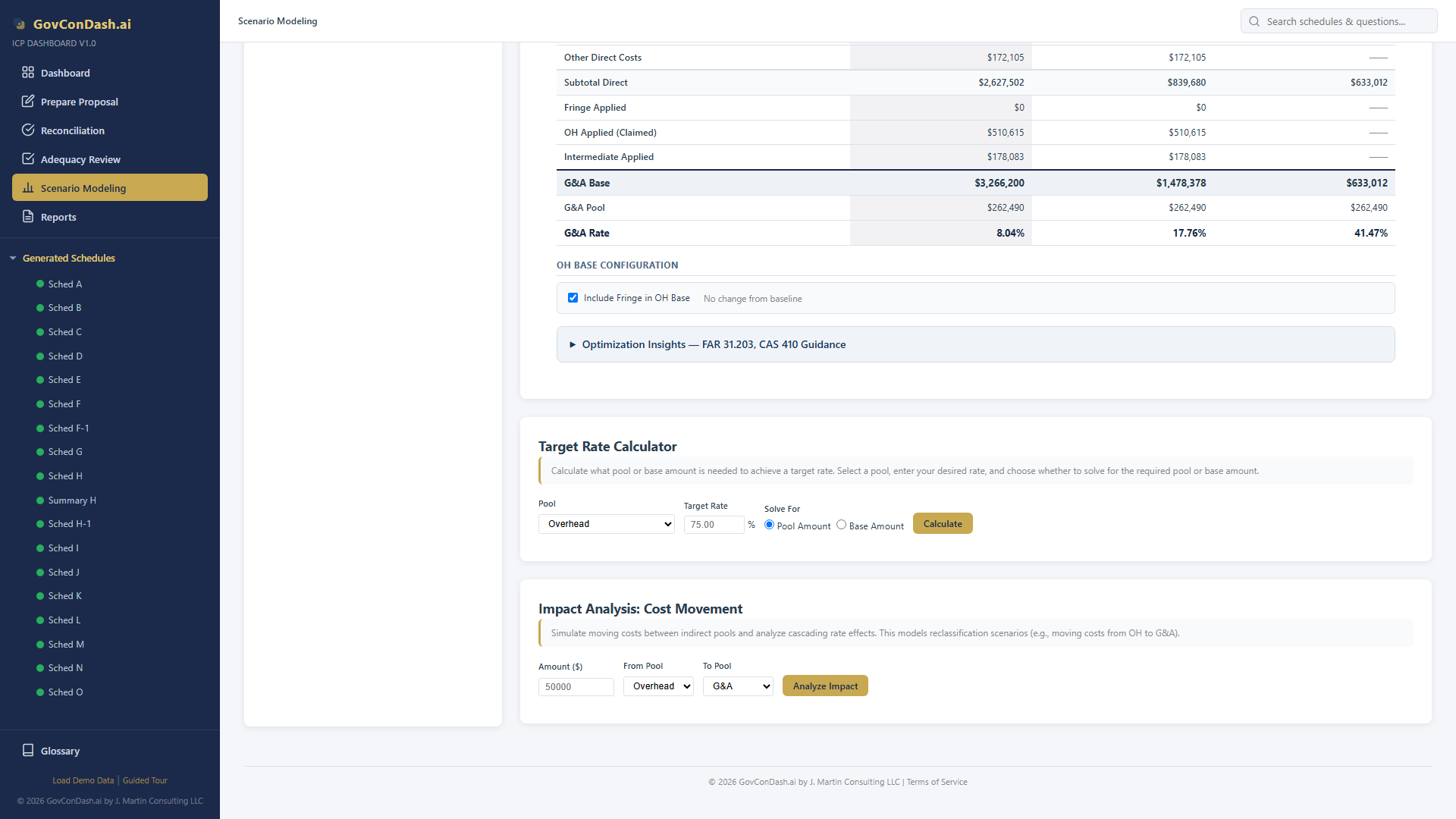

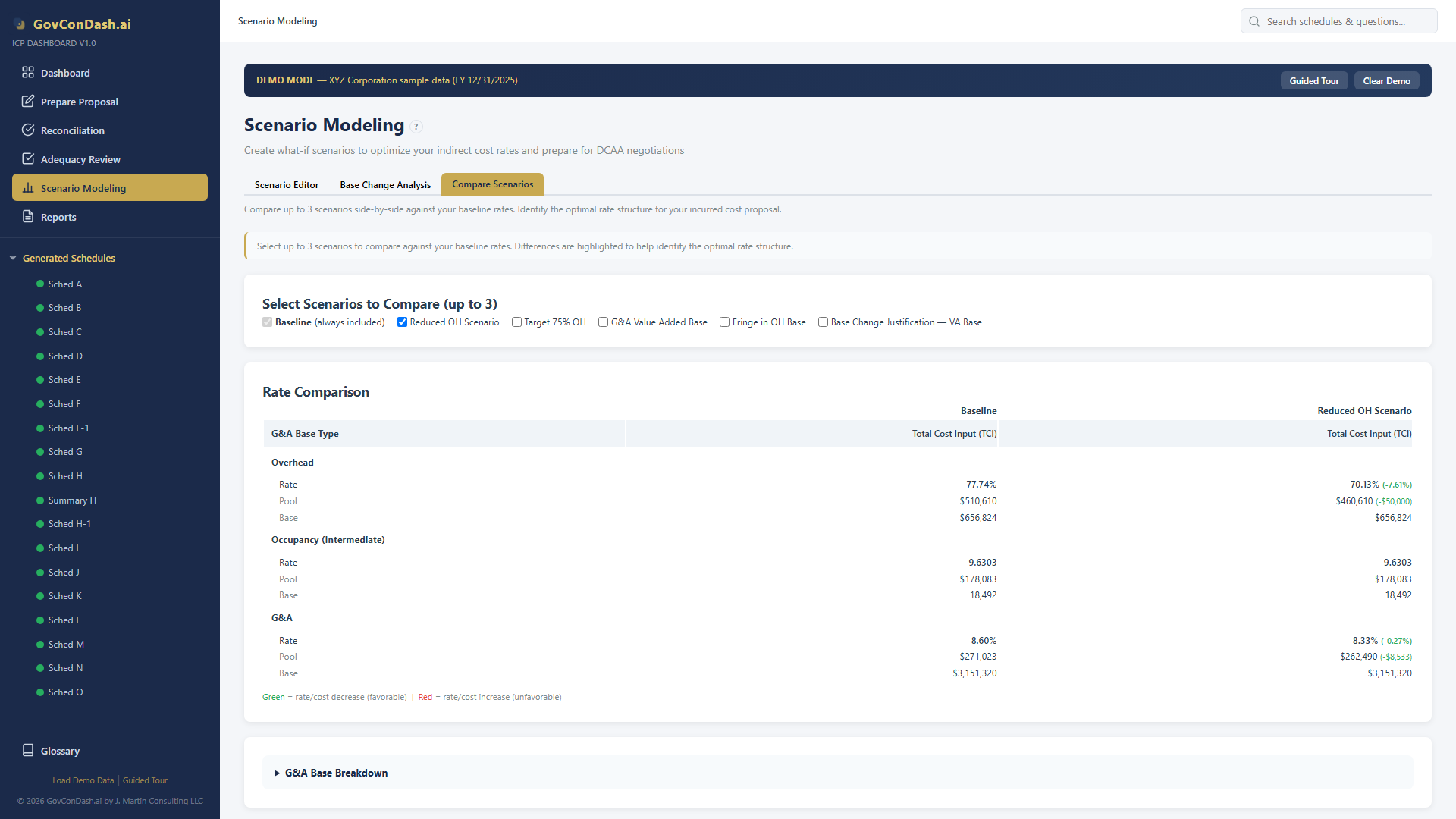

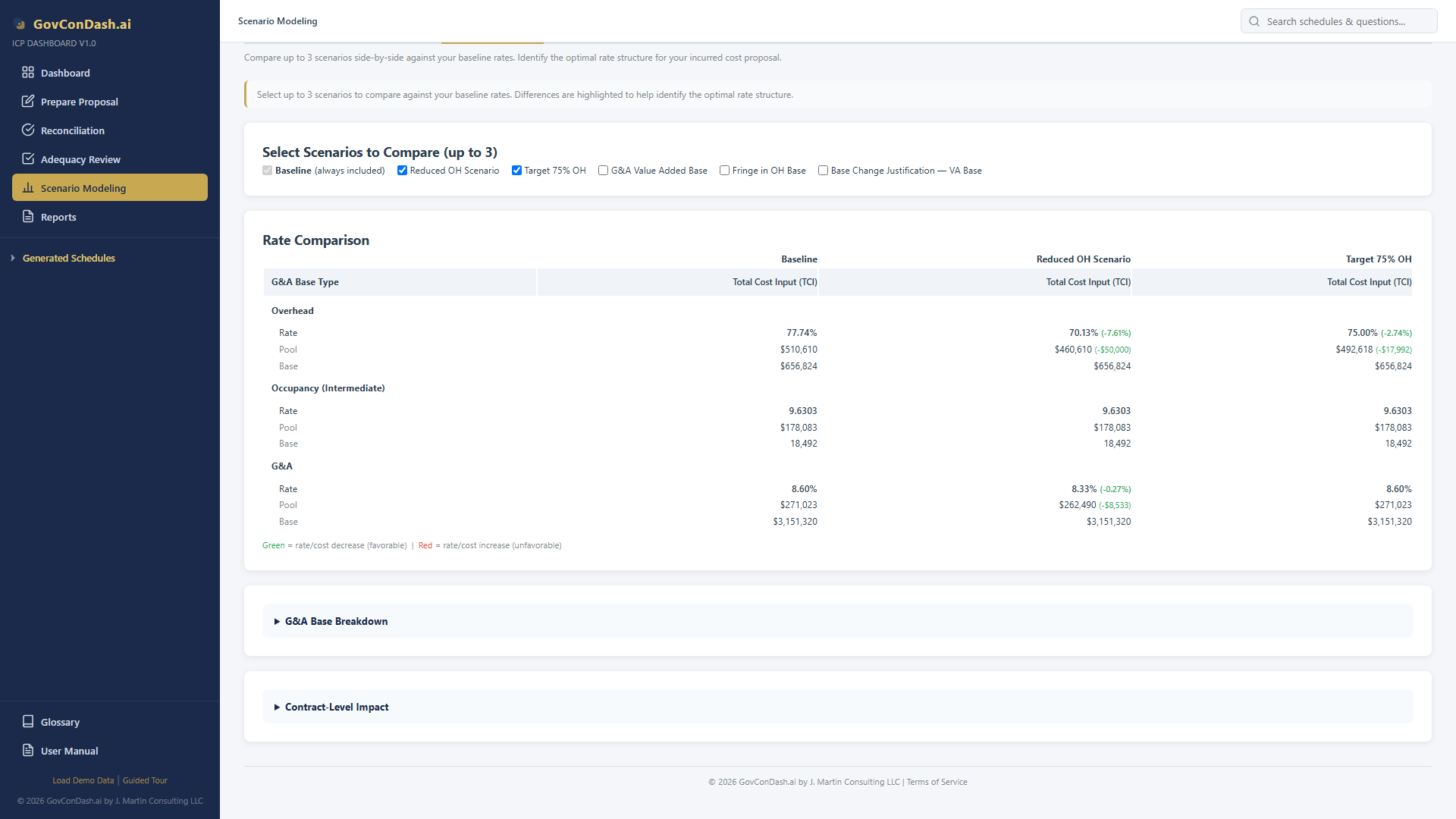

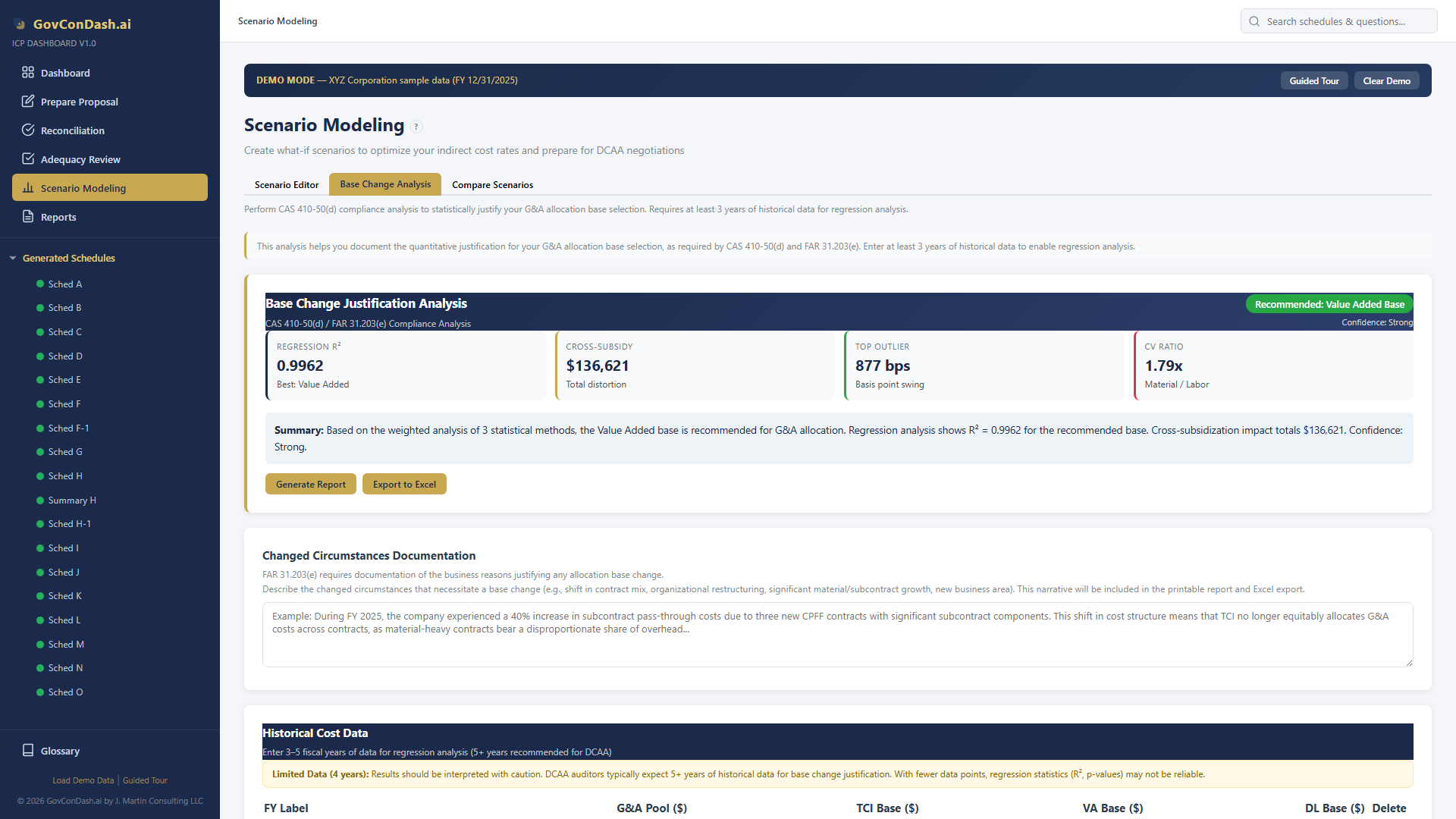

If you determine that a different G&A base type would be more equitable, you need documented evidence to justify the change to your DCAA auditor and Administrative Contracting Officer (ACO). The Base Change Analysis tab provides a comprehensive analytical framework with four complementary methods.

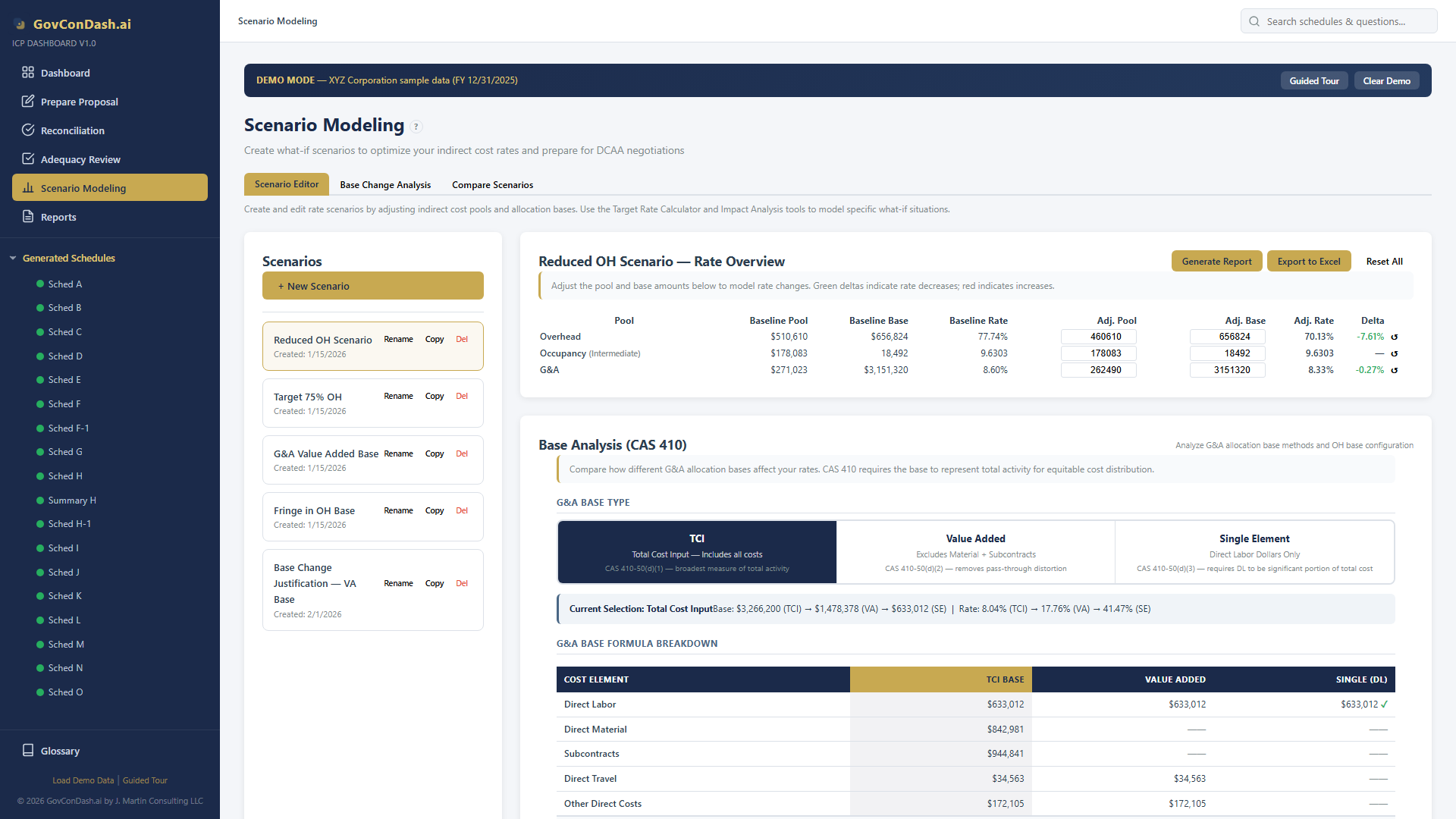

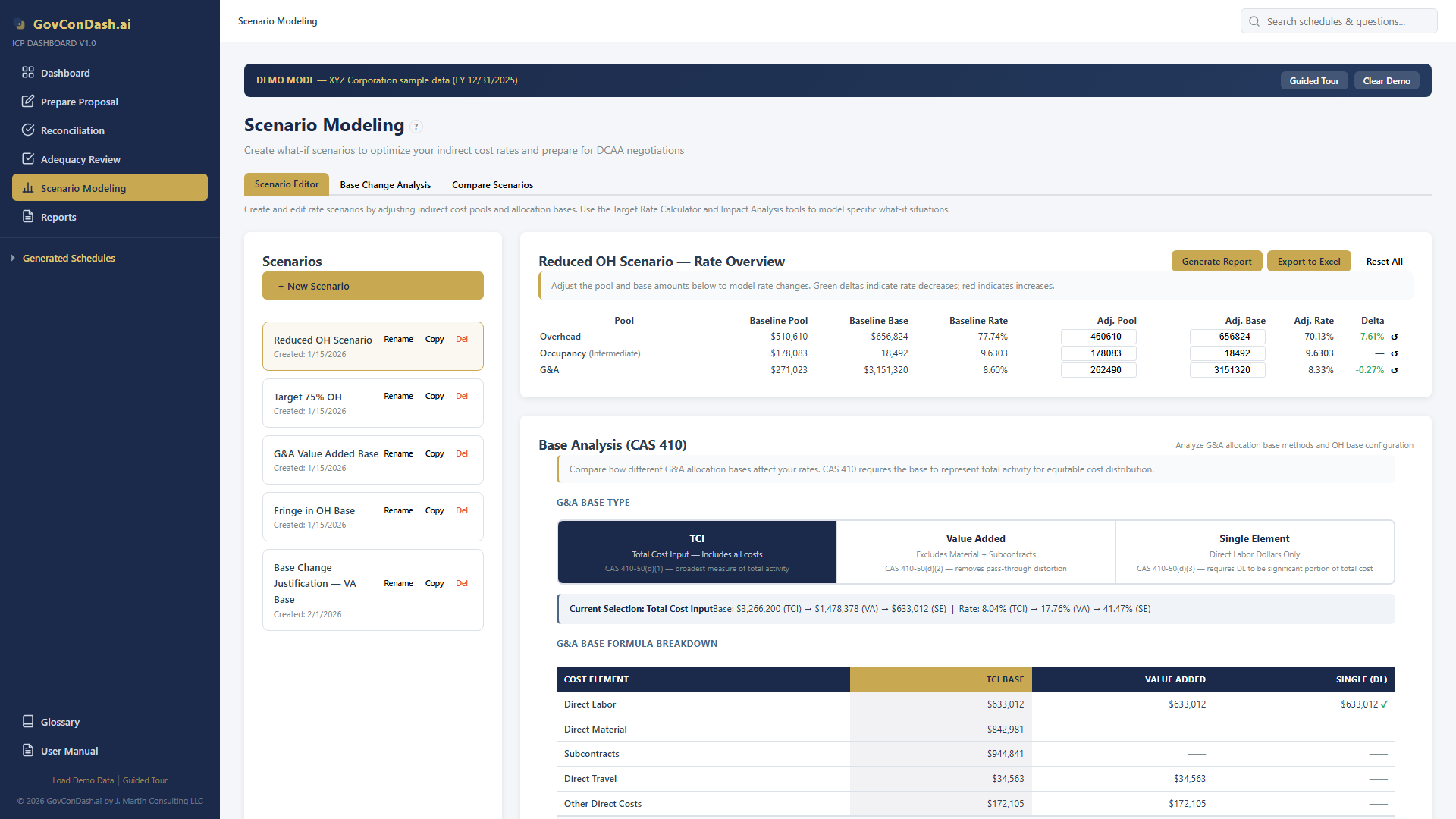

Access it by clicking the “Base Change Analysis” tab at the top of the Scenario Modeling page.

Base Change Analysis tab with summary card, historical data, and analysis panels

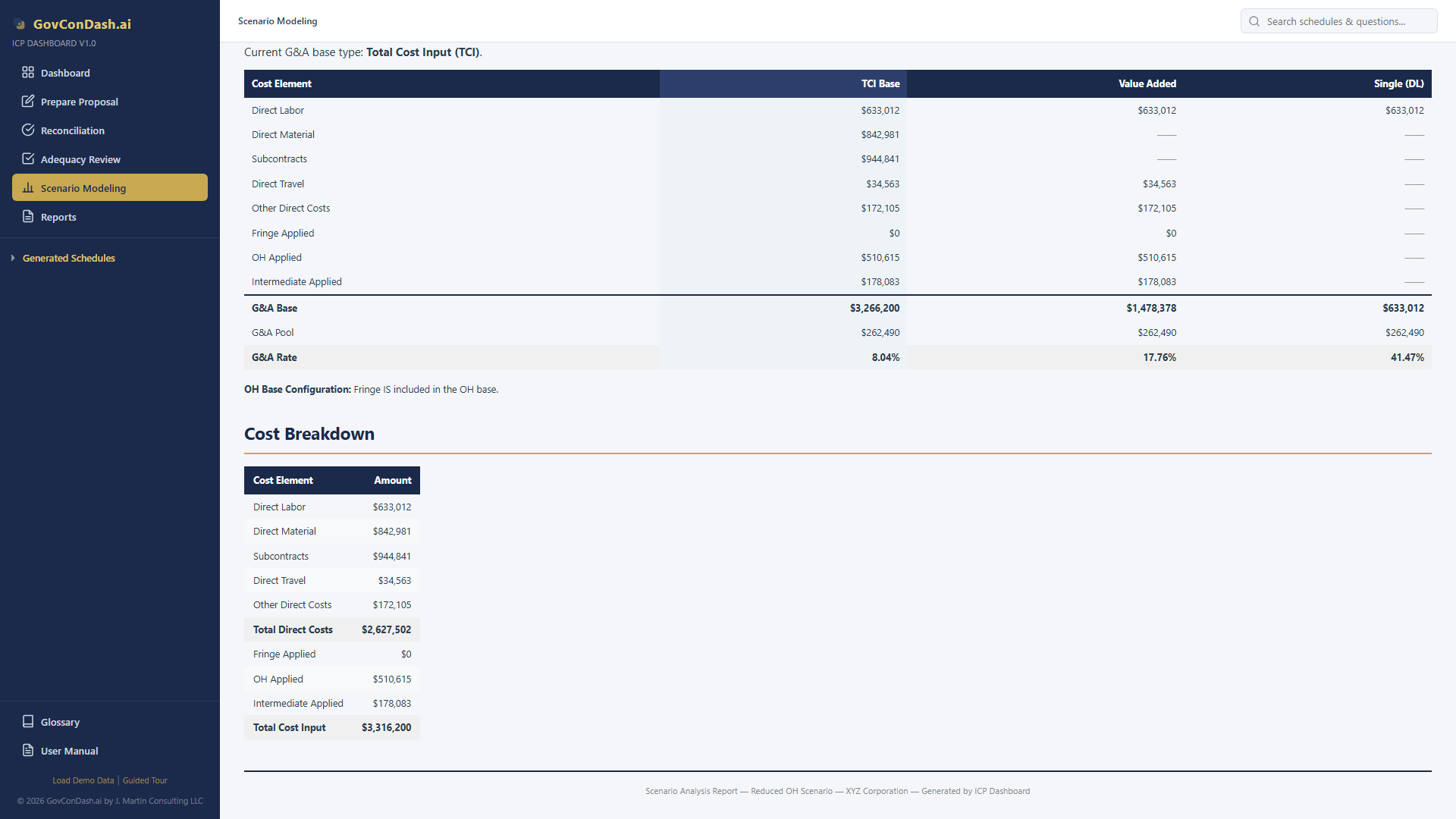

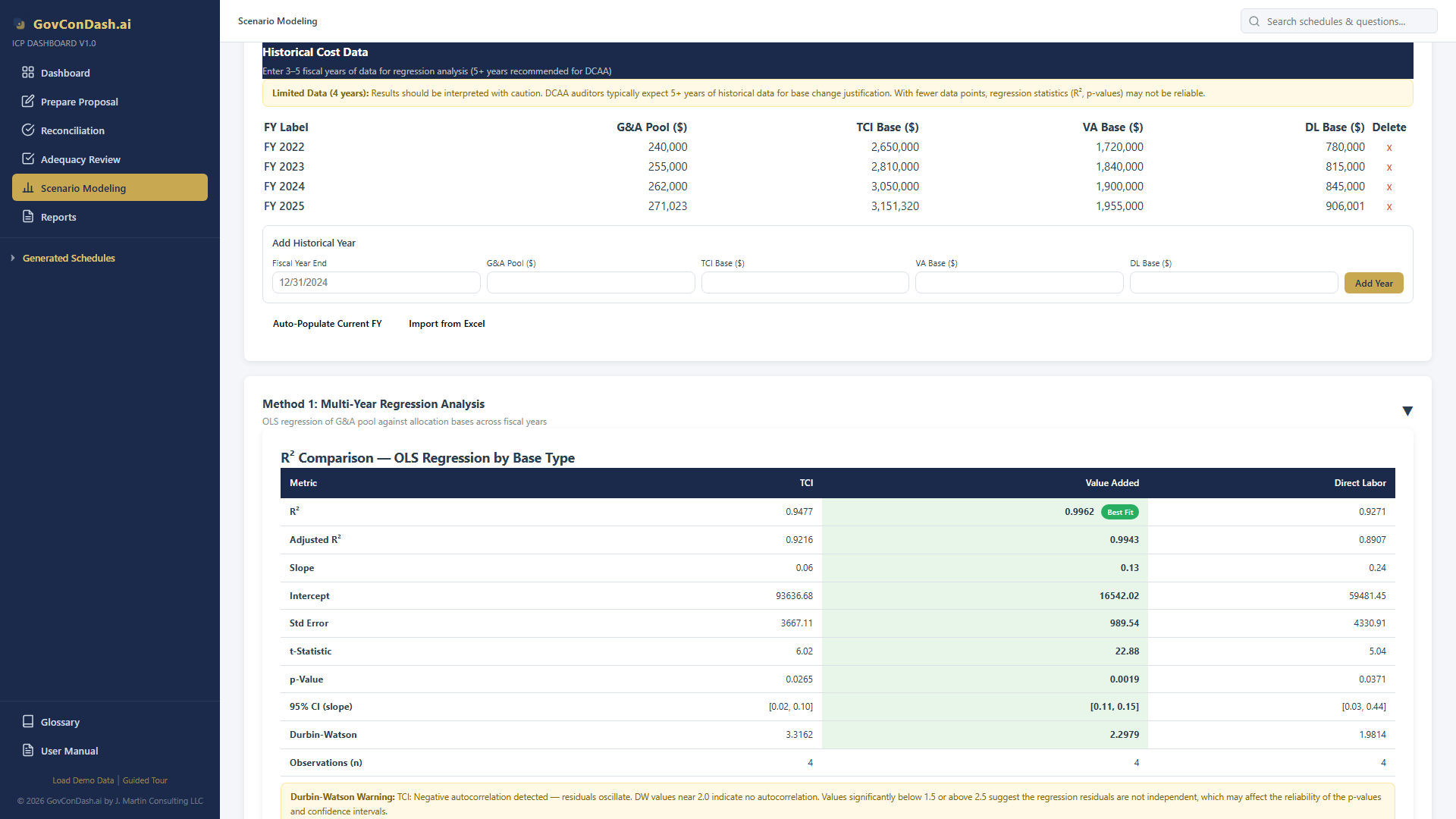

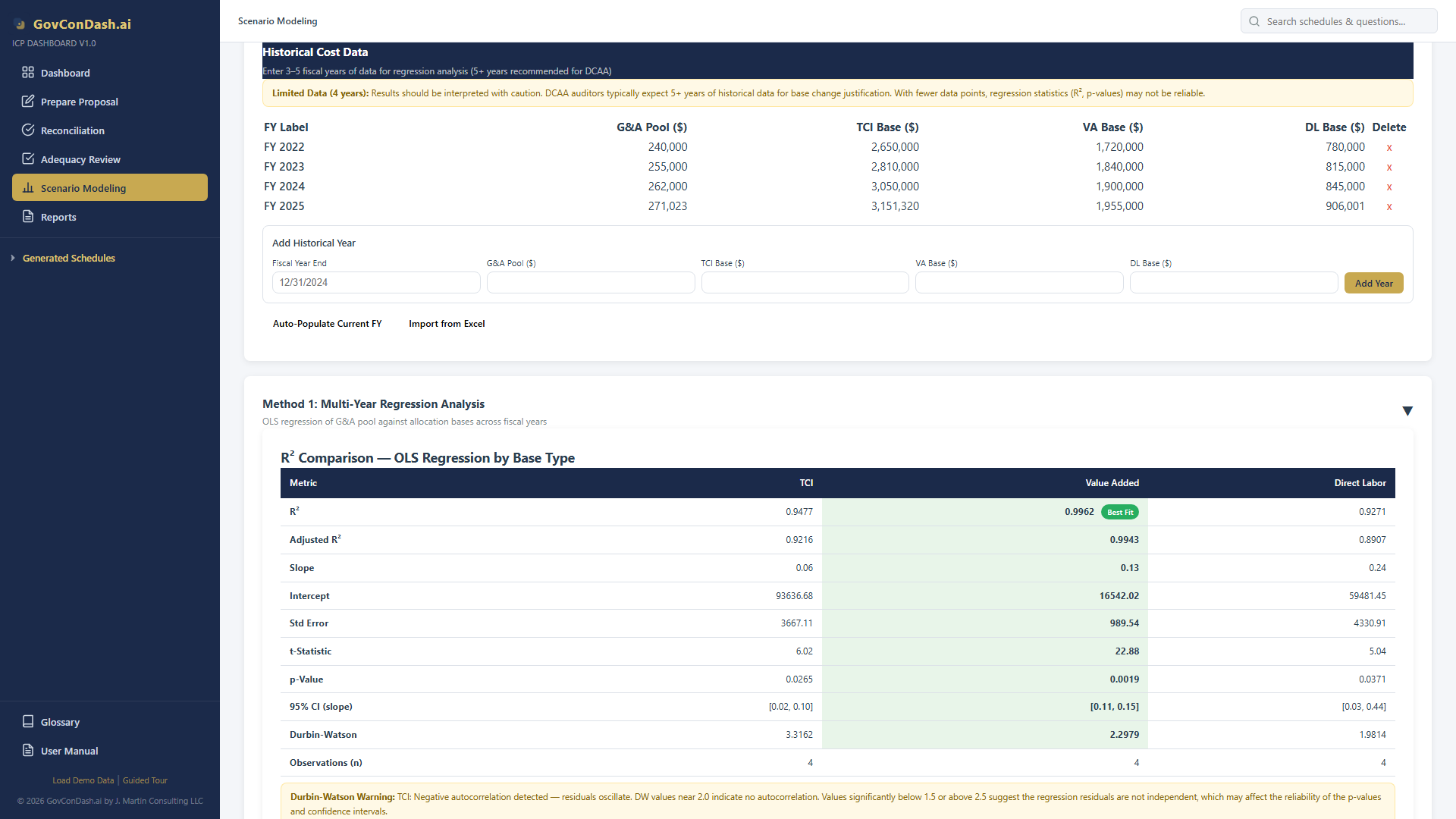

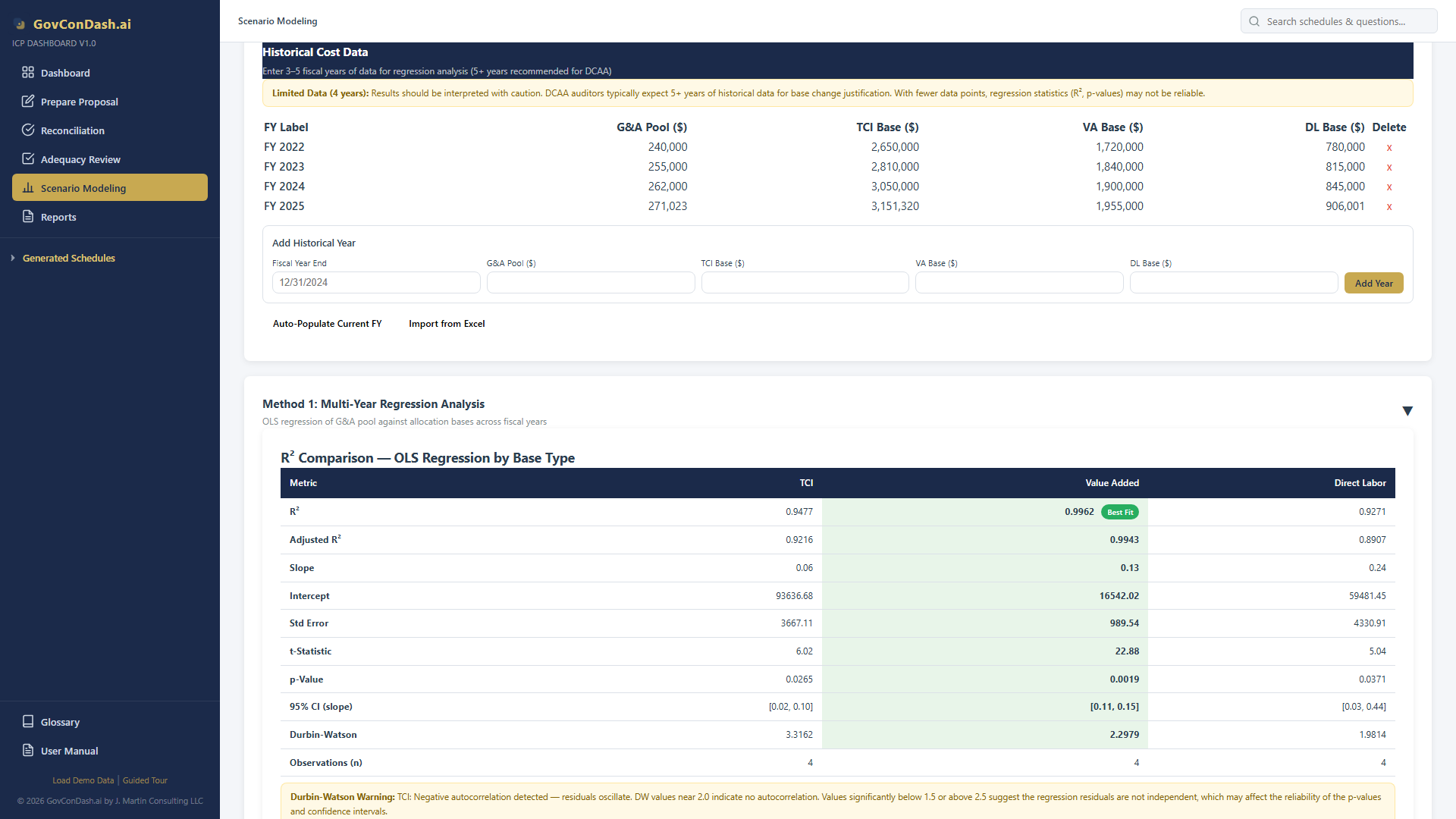

7.1 Entering Historical Data

The regression analysis requires multiple years of historical G&A pool and base data. For each fiscal year, enter:

- FY Label — e.g., “FY 2025”

- G&A Pool ($) — Total G&A indirect cost pool for that year

- TCI Base ($) — Total Cost Input allocation base

- Value Added Base ($) — TCI minus material and subcontracts

- Direct Labor Base ($) — Total direct labor dollars

You can also import from prior-year ICE workbooks (upload Excel files and the system parses Schedule B and GL data) or click “Use Current Year Data” to auto-populate from your generated schedules.

Tip: Data Quality

DCAA typically expects

5+ years of historical data for strong statistical evidence. The minimum for regression analysis is 3 years. More data points produce more reliable R² values and narrower confidence intervals.

Historical data entry form with fiscal year entries and import options

7.2 Documenting Changed Circumstances

FAR 31.203(e) requires documenting the changed circumstances that warrant a base change. Use the text area to describe business changes — for example, significant growth in subcontract spending, organizational restructuring, new product lines, or major contract type shifts. This narrative is included in exported reports.

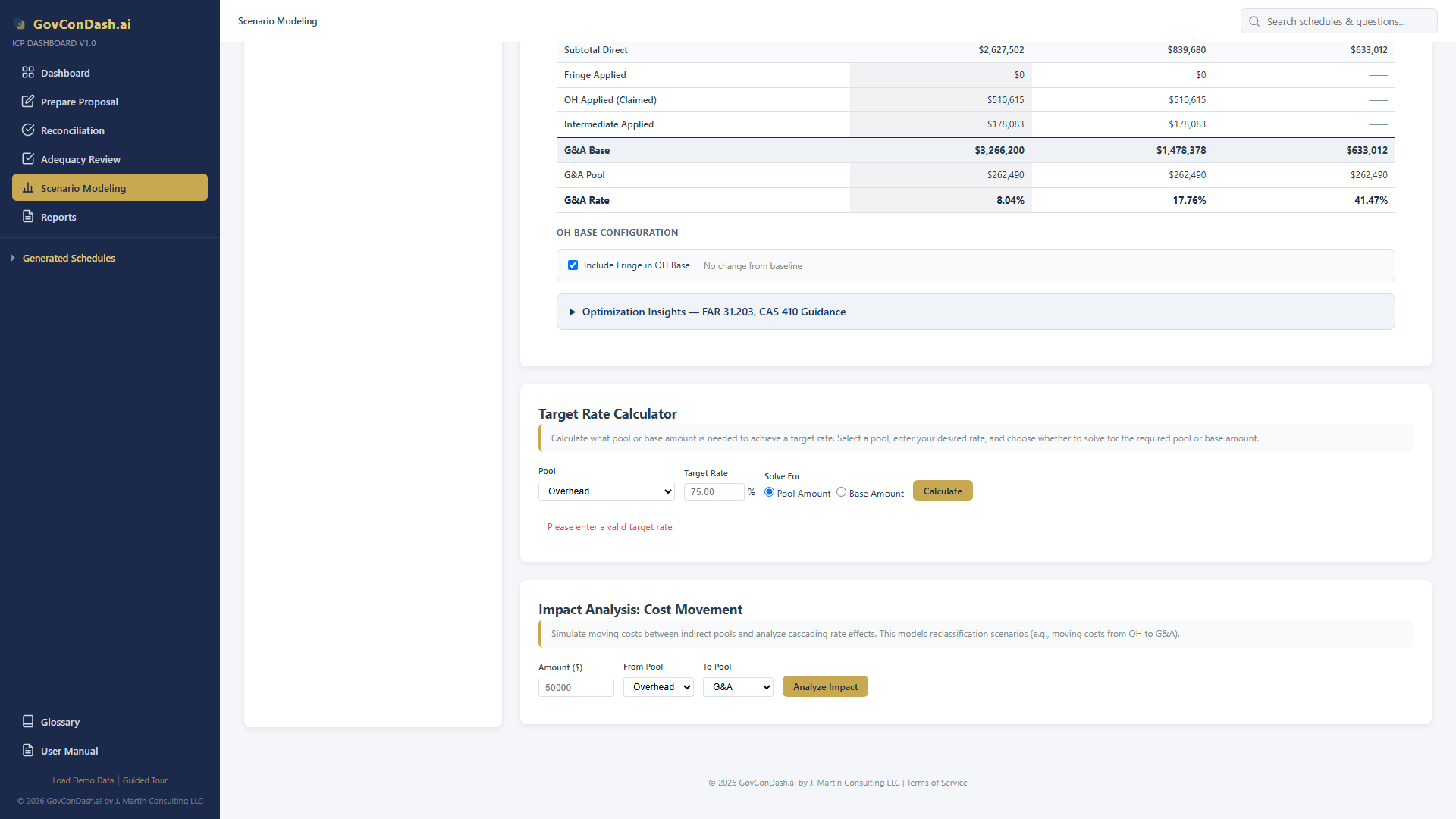

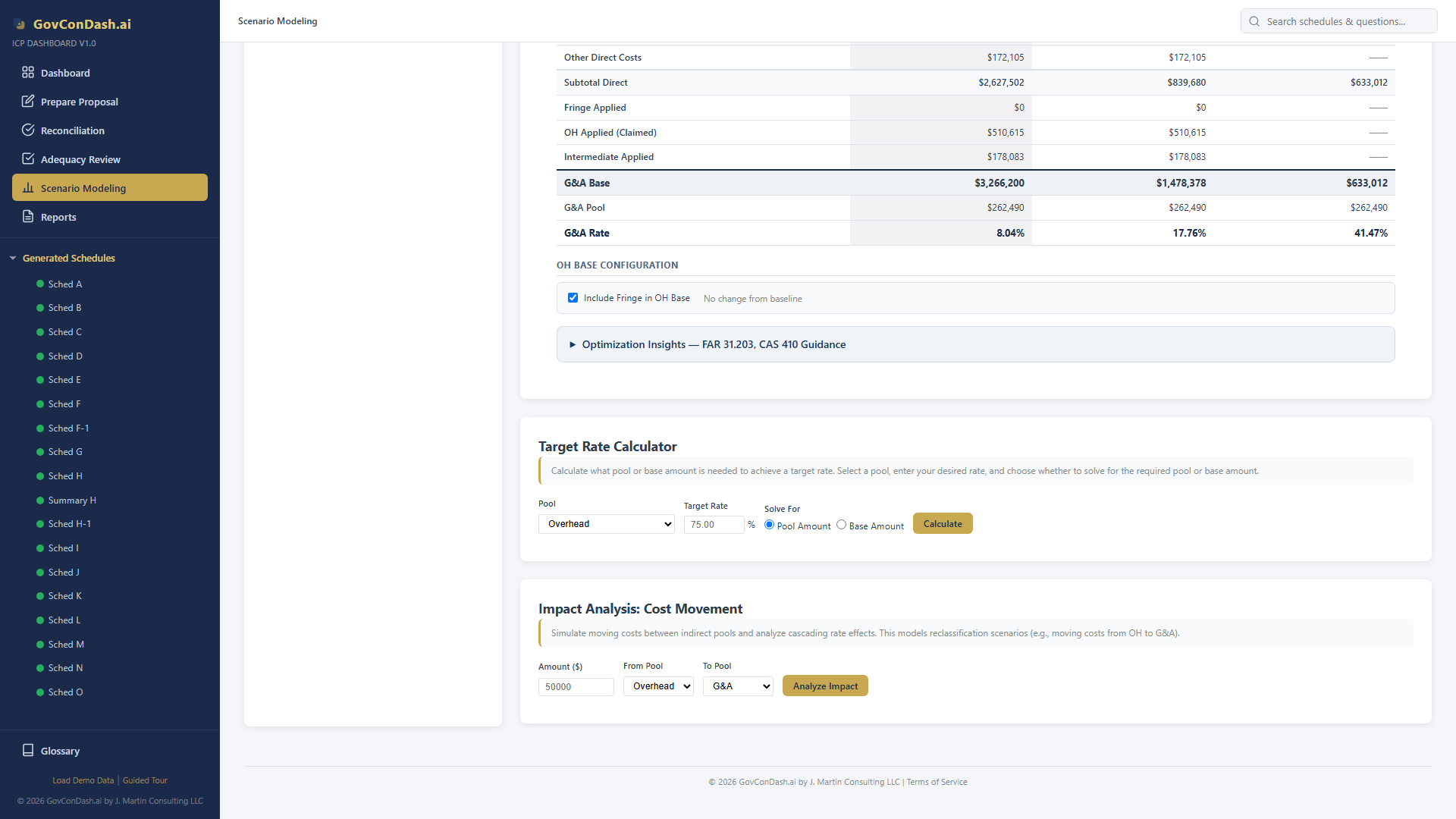

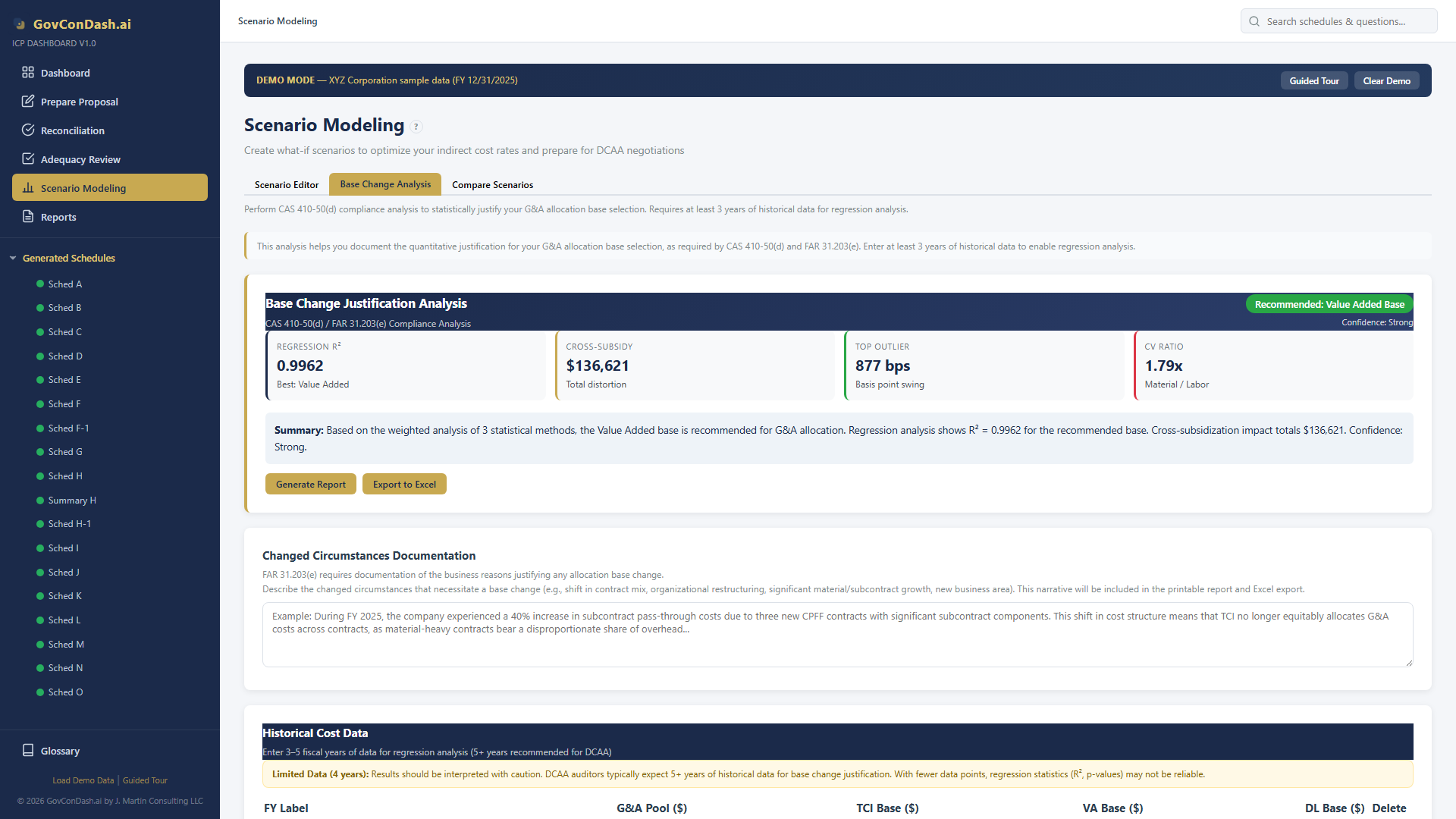

7.3 Analysis Summary

At the top of the analysis tab, a summary card shows the overall recommendation with a confidence badge:

- Recommended Base — The base type supported by the most evidence

- Confidence Level — Strong (all methods agree), Moderate (2 of 3), or Weak (mixed signals)

- Four metrics — Best R², cross-subsidization amount, top outlier swing (basis points), CV ratio

Analysis summary showing recommended base type, confidence level, and key metrics

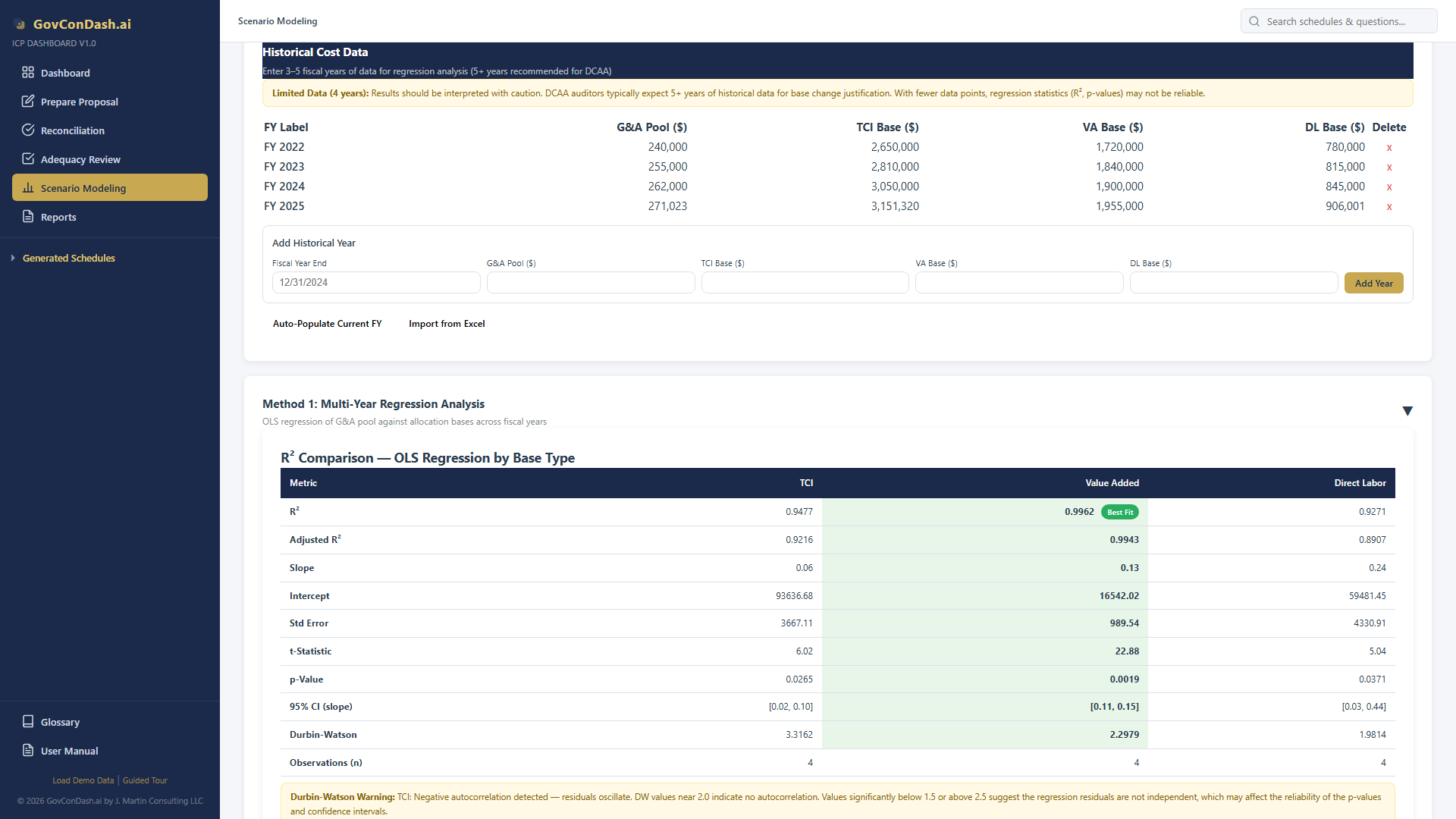

7.4 Method 1 — Multi-Year Regression (OLS)

Ordinary Least Squares regression tests how well each allocation base (TCI, Value Added, Direct Labor) predicts the G&A pool over time. The base with the highest R² is the best statistical predictor.

- R² — Goodness of fit (0 to 1). Higher is better. >0.90 = strong, 0.70–0.90 = moderate, <0.70 = weak

- p-value — Statistical significance. <0.05 = significant, <0.10 = marginally significant

- Confidence intervals — Range within which the true slope likely falls (95% confidence)

- Scatter plots — Visual representation with regression lines and confidence bands

Three scatter plots comparing TCI, Value Added, and Direct Labor bases vs. G&A pool with regression lines and R² values

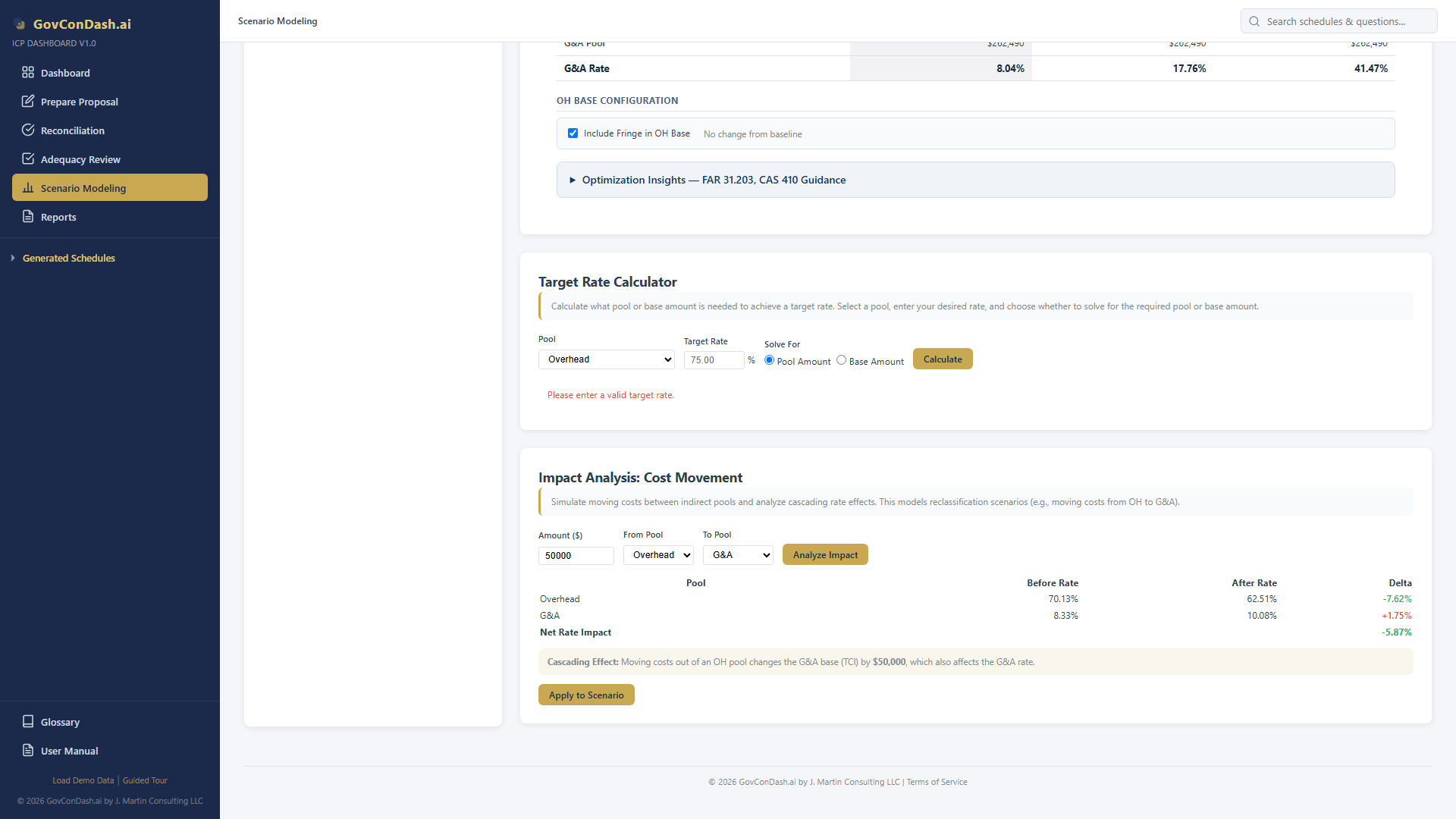

7.5 Method 2 — Comparative Rate Impact Analysis

This method examines how each base type affects G&A allocation at the individual contract level. It computes the G&A rate and allocation amount for every contract under each base type and identifies cross-subsidization — contracts that would pay more or less G&A under different bases.

It also flags the CAS 410-50(d)(3) threshold: if direct labor is less than 15% of TCI, using Single Element as the base is questionable because labor is not a significant portion of total activity.

Rate Impact Analysis showing contract-level G&A allocation under each base type

7.6 Method 3 — Sensitivity & Outlier Analysis

The sensitivity analysis looks at how concentrated material and subcontract costs are across your contract portfolio, helping assess whether pass-through distortion justifies a Value Added base:

- Pareto concentration — What percentage of total material/sub is concentrated in the top contracts?

- Herfindahl index — Market-style concentration metric applied to cost distribution

- Coefficient of variation — Compares rate variability across base types (lower CV = more stable)

- Rate stability ranking — Which base produces the most stable rates over time?

Sensitivity and Outlier Analysis with Pareto concentration and CV comparison

7.7 Reading the Recommendation

The tool aggregates findings from all three methods using a voting system. Each method contributes its recommended base type, and the overall recommendation reflects the consensus:

- Strong confidence — All methods agree on the same base type

- Moderate confidence — Two of three methods agree

- Weak confidence — Methods recommend different bases (mixed signals)

Important Disclaimer

This tool provides analytical support for your base change justification. It does

not replace professional judgment, consultation with your cost accountant, or formal review by your DCAA auditor and ACO. Always consult qualified professionals before submitting a base change request.