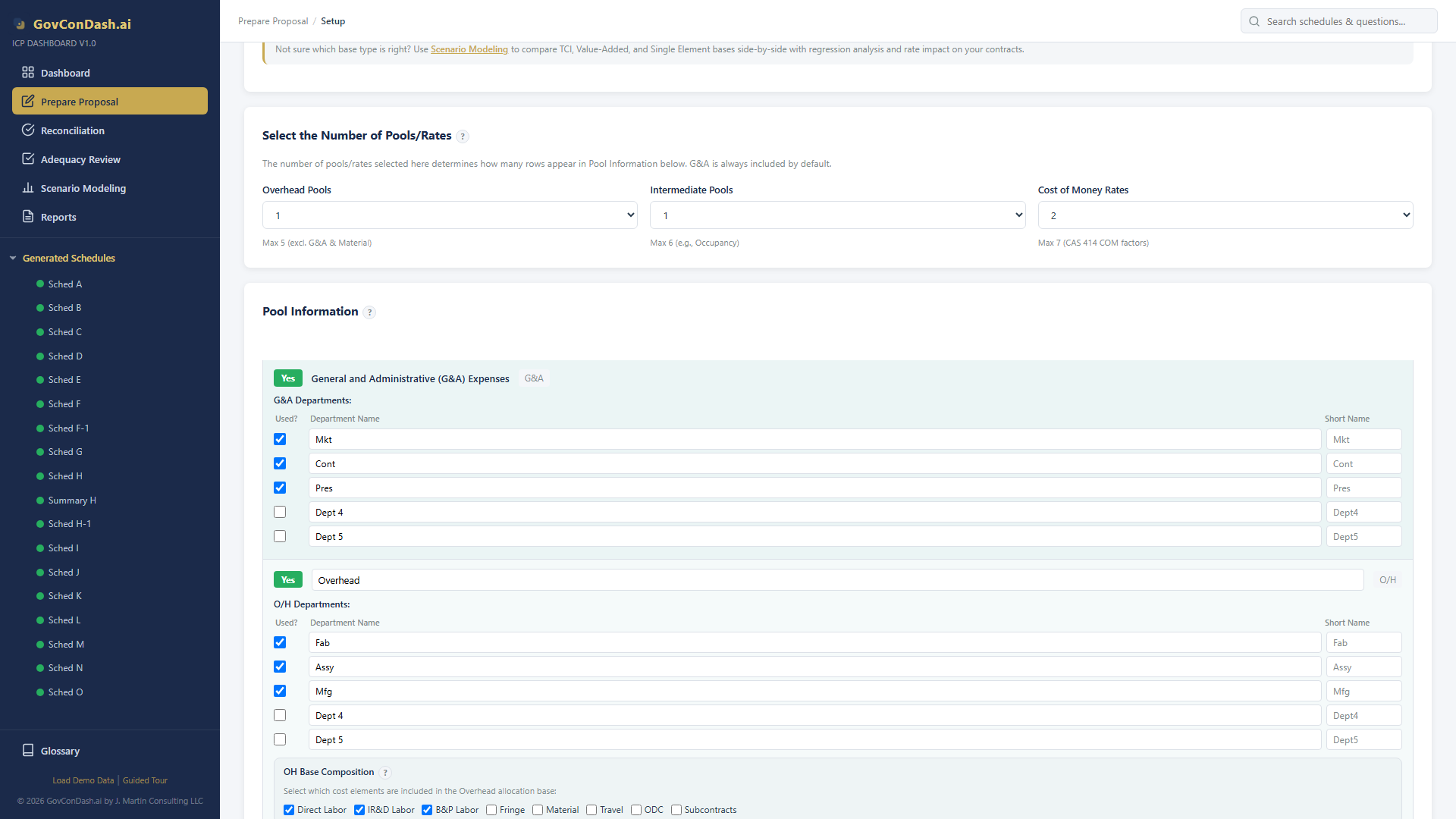

Two-Tier Structure (Fringe in Overhead)

Some contractors, particularly smaller firms, bundle fringe costs into the overhead pool. This simplifies the rate structure to just two tiers (Overhead + G&A) but produces a significantly higher overhead rate.

- Two Pools — Overhead rate (includes fringe) + G&A rate. Fewer pools to manage but less cost visibility.

- Higher Overhead Rate — Fringe costs (FICA, health insurance, PTO, retirement) are added to the overhead pool, substantially increasing the overhead rate percentage

- Higher Wrap Rate — Fringe moves from the base to the pool, shrinking the denominator and growing the numerator. The resulting wrap rate is typically higher than three-tier.

- Dashboard Setting — Disable "Fringe as Separate Rate" in Setup. Fringe costs flow into the overhead pool on Schedule C. Optionally enable "Fringe in Overhead Base" to add fringe back into the base.