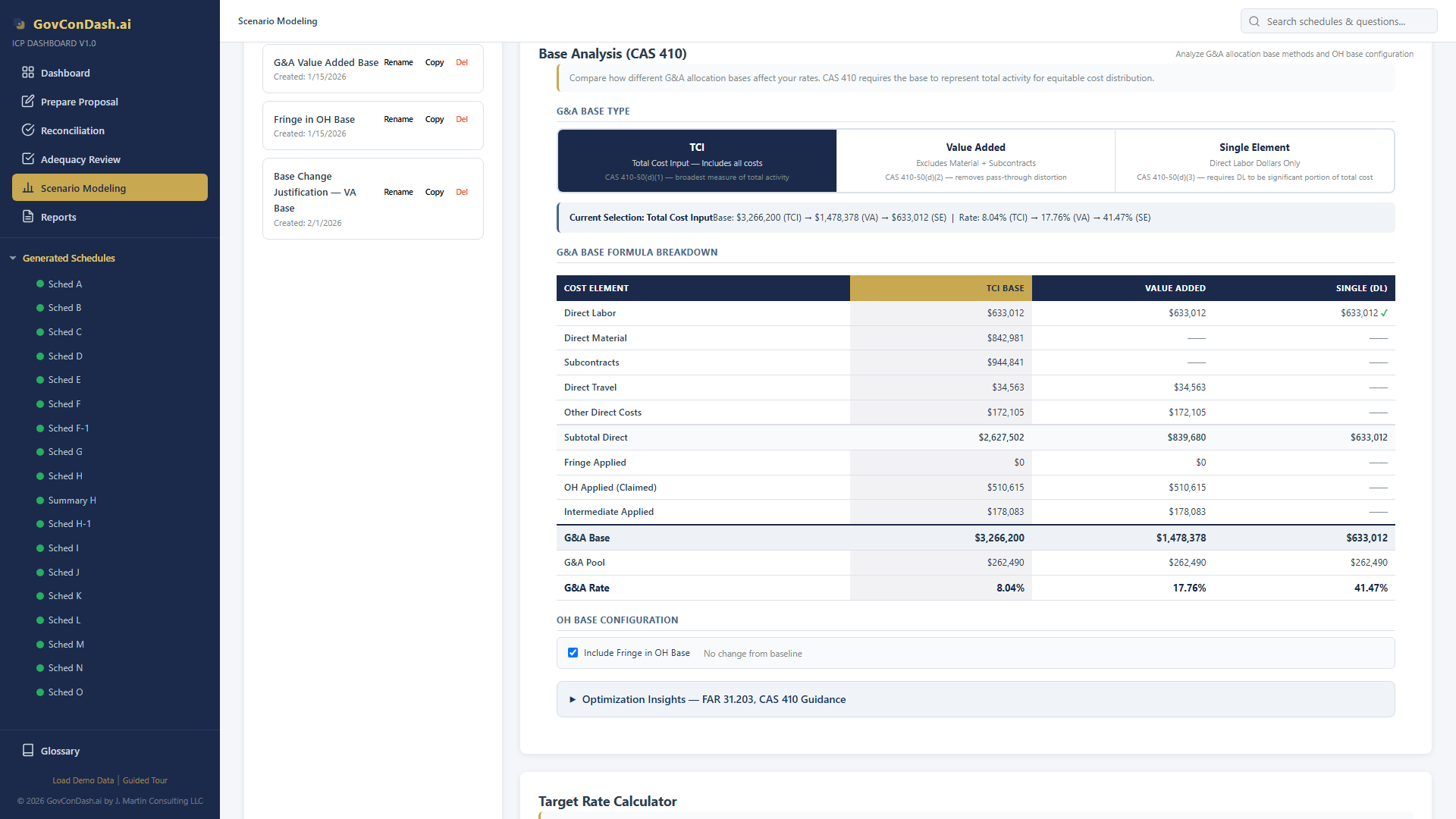

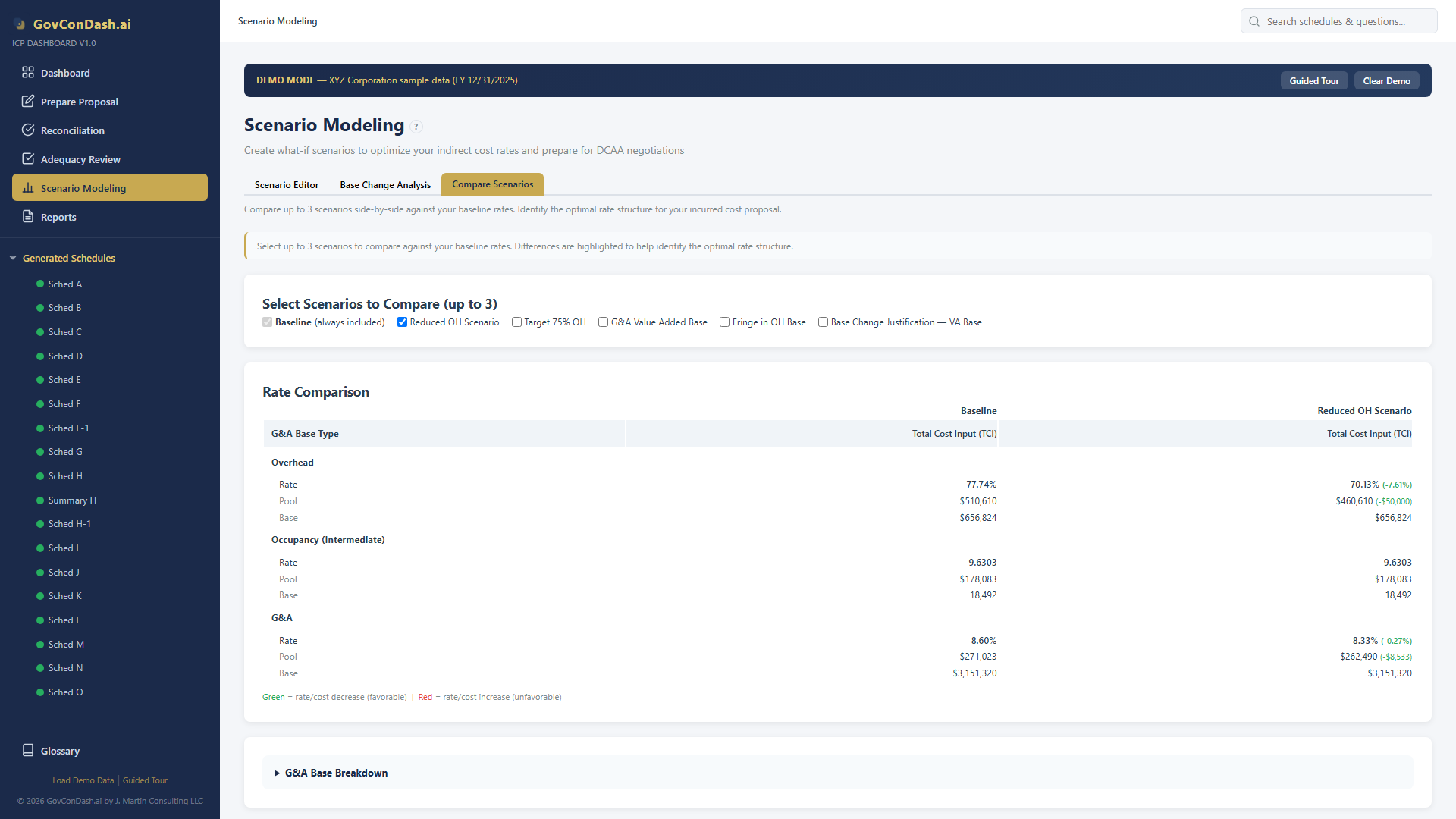

Side-by-Side Rate Comparison

Create up to three scenarios and compare them against your baseline. Each scenario can use a different G&A base type, pool adjustments, or cost reclassifications — and instantly see the impact on every rate.

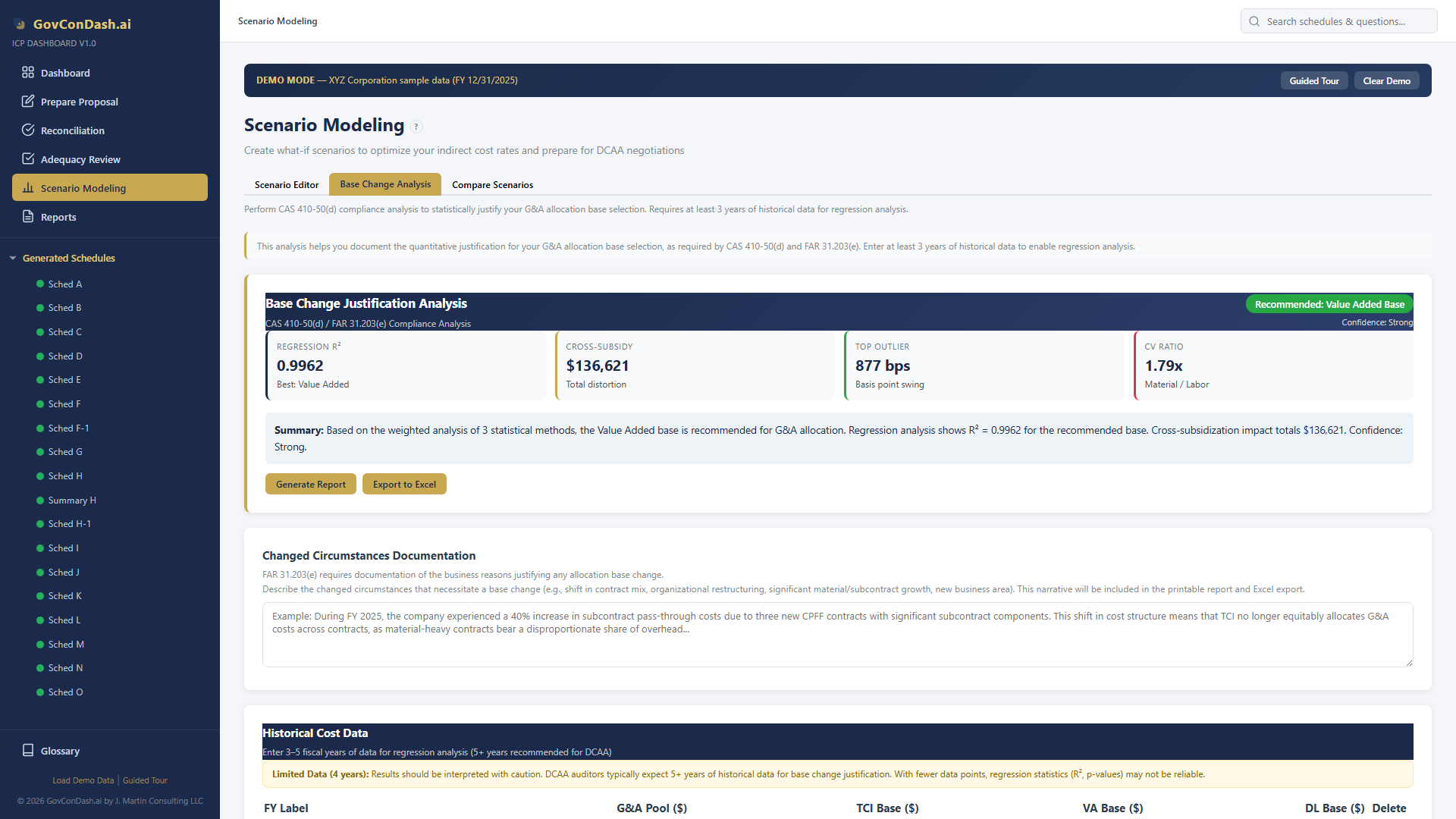

- Base Type Toggle — Switch a scenario between TCI, Value Added, and Single Element to see how the G&A rate changes under each allocation method

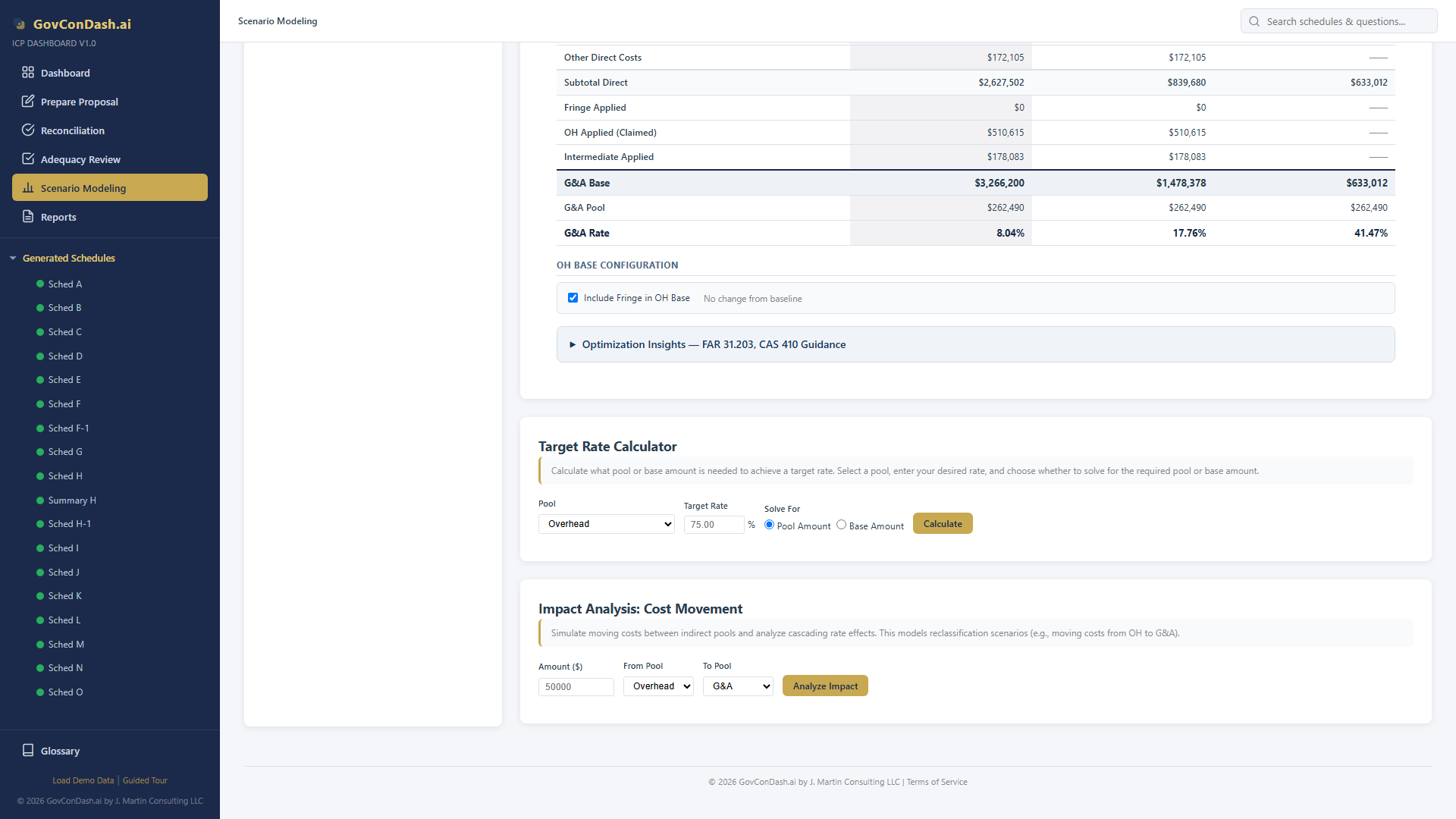

- Pool Adjustments — Move costs between OH and G&A pools and see cascading rate effects in real time

- Delta Highlighting — Rate increases and decreases are color-coded so you can spot the impact at a glance

- Contract-Level Preview — See how G&A allocation shifts across individual contracts under each scenario